ACH payment growth continues to underscore the importance of electronic funds transfers in the modern payments ecosystem. As businesses and consumers increasingly shift away from paper-based payment methods, the ACH network remains a critical rail for payroll, bill payments, business transactions, and peer-to-peer transfers. Recent transaction growth highlights how ongoing enhancements to the network are helping it remain competitive even as faster payment alternatives gain traction.

One of the most notable developments has been the rise of digital payment channels and business-to-business transactions. As organizations continue digitizing payment processes, ACH has benefited from the migration away from checks and other manual payment methods. At the same time, improvements such as same-day settlement are making the network more attractive for use cases that previously required faster, more expensive payment options.

ACH transactions are electronic funds transfers (EFT) that are processed by the network. This network is overseen by the National Automated Clearing House Association (NACHA). Transactions typically take one to two business days to process, but same-day transactions are also available for an additional fee. ACH transactions are used for a variety of purposes, including direct deposit of payroll and government benefits, bill payments, and peer-to-peer payments.

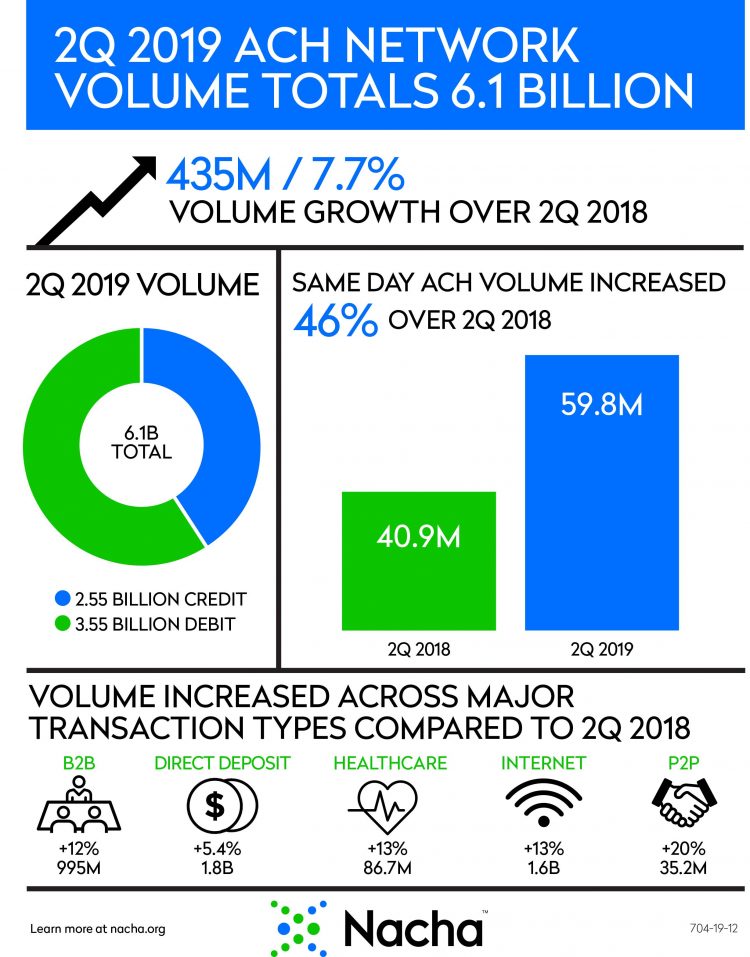

NACHA announced significant transaction growth in the second quarter. Two stand-out categories were web-initiated transactions and B2B transactions. Digital Transactions reported that total volume for the quarter reached 6.1 billion transactions, an increase of 7.7% from the same period a year earlier. The network has consistently posted strong growth as features such as same-day ACH processing continue to gain adoption.

Internet-initiated payments were a major contributor, totaling 1.6 billion transactions and increasing 13% year over year. B2B payments also delivered strong results, rising 12% to 995 million transactions. Because overall payment transaction growth tends to be relatively modest, much of this increase likely reflects continued displacement of paper checks and, in some online scenarios, certain card-based transactions.

Same-day ACH also posted impressive growth during the quarter. Volume increased 46% to 59.8 million transactions, encompassing both credits and debits. Since its introduction in 2016 and subsequent expansion, same-day ACH has become an increasingly important component of the broader faster payments movement. Additional processing windows have further enhanced its utility and accessibility.

This growth may indicate that same-day ACH is replacing some wire transfer activity as well as traditional next-day ACH transactions. For many organizations, it offers a balance between speed and cost that can be more attractive than other payment methods.

ACH transactions are electronic funds transfers (EFT) that are processed by the network. This network is overseen by the National Automated Clearing House Association (NACHA). Transactions typically take one to two business days to process, but same-day transactions are also available for an additional fee. ACH transactions are used for a variety of purposes, including direct deposit of payroll and government benefits, bill payments, and peer-to-peer payments.

NACHA announced significant transaction growth in second quarter. Two stand-out categories were web initiated transactions and B2B transactions. Digital Transactions reported:

Total volume for the quarter came to 6.1 billion transactions, an increase of 7.7% from the same three months last year, according to Nacha, the Herndon, Va.-based organization that administers the 45-year-old network. The system has been steadily posting 5%-plus quarterly growth rates in recent years as new features such as same-day ACH processing have been introduced.

Contributing to the growth for the latest quarter were transactions Nacha classifies as Internet-initiated payments. These totaled 1.6 billion, up fully 13%. Also helping out were B2B payments, which rose 12% to 995 million.

Since the number of transactions in total rarely increases much, this growth is likely to have come from checks and in the case of internet initiated payments, some card transactions were likely displaced.

Same day ACH also saw real growth in 2nd quarter:

Same-day volume, which is part of the faster-payments trend and has been closely watched since the ACH introduced same-day credits in 2016, jumped 46% to 59.8 million. This volume includes both credits and debits, which were added in 2017. Nacha expects to add a third processing window in March 2021 as part of its years-long effort to facilitate same-day processing.

This volume is likely to be replacing wire transfers and “slow” ACH.

As real-time payments start to grow and get closer to matching the ubiquity of ACH, we will want to watch if same day ACH turns out to be a stepping stone to real-time payments or if the two payments, with notable feature differences, are distinct and operate in specific use cases. We still are a long way off for this type of activity to be noticed and in the meantime, same day ACH and ACH generally is enjoying great growth.

The continued expansion of ACH payment growth demonstrates the enduring relevance of the ACH network despite the emergence of newer payment rails. Strong gains in web-initiated payments, B2B transactions, and same-day ACH adoption suggest that businesses and consumers continue to value a payment system that combines broad reach, reliability, and improving speed.

Looking ahead, the relationship between same-day ACH and real-time payments will be worth monitoring. While some overlap exists, each payment type offers distinct features that may ultimately serve different use cases. Until real-time payments achieve broader ubiquity, ACH—and particularly same-day ACH—is well positioned to remain a major driver of electronic payment innovation and growth.

Here’s a link to NACHA’s infographic outlining the details around second quarter’s growth.

Overview by Sarah Grotta, Director, Debit and Alternative Products Advisory Service at Mercator Advisory Group