In recent years, earned wage access (EWA) has grown in popularity as a way for employees to receive wages on-demand. But in a stunning blow to the community of EWA providers who debit, the Consumer Financial Protection Bureau (CFPB) released an advisory opinion on Nov. 30, 2020, explicitly excluding debiting practices from safe harbor. Instead, it validated the employer-based, non-recourse approach that companies like DailyPay have pioneered and championed for years.

To learn more about the significance of the CFPB’s advisory opinion, its follow-up order, and what they mean for earned wage access providers and the employers that work with them, PaymentsJournal sat down with Jason Lee, CEO and co-founder of DailyPay, and Sarah Grotta, Director of Debit and Alternative Products Advisory Service at Mercator Advisory Group.

What is earned wage access?

Earned wage access, commonly abbreviated as EWA, goes by many names, including early wage access, on-demand pay, or daily pay benefit. All of these terms refer to an employee being able to access the money they’ve earned before their employer’s scheduled payday. “In a nutshell, [EWA] is broadly defined as an industry that works with employers and enables their employees to access their pay on their own schedule,” explained Lee.

A common earned wage access model is a provider giving funds to an employee then requiring the employee to pay it back, which can be done through a variety of means such as a bank account debiting or directed payroll deduction.

Credit requires an employee obligation to repay, so much of the question has been who has the obligation to repay EWA funds. The employer-integrated context has both informational verification (through data syncing) and direct funds-flow integration (through payroll), so providing someone access to their own money they have already earned is not credit-like in nature.

There are several models that do not rely on employees paying back through an employer payroll deduction, but the focus of the CFPB’s advisory opinion and follow-up order was to address certain EWA business practices in narrow circumstances.

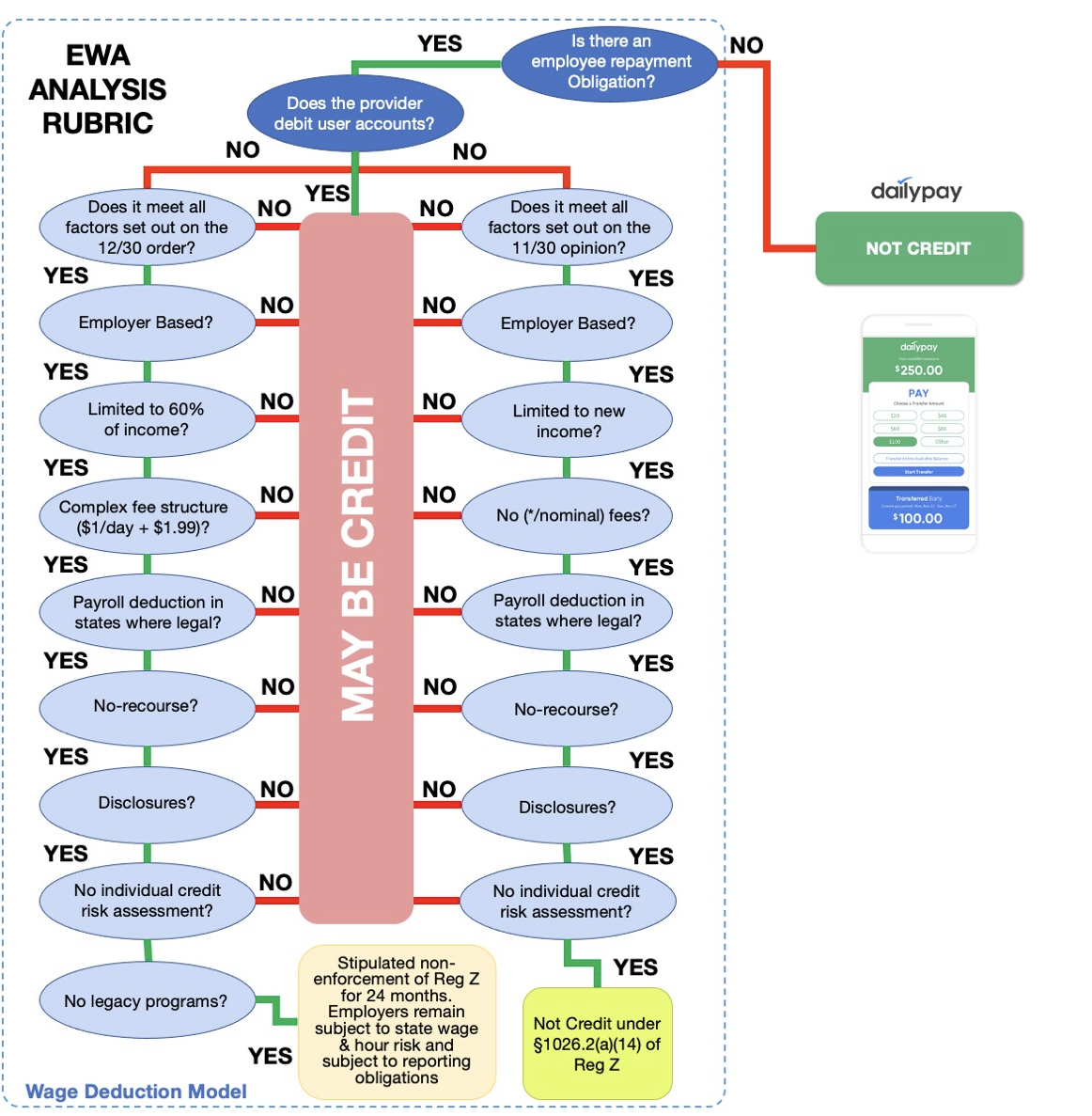

The CFPB’s November 2020 advisory opinion

The CFPB’s advisory opinion stated that organizations providing earned wage access that meet a set of conditions will not be deemed credit. It also stipulated how employees can pay back. To break down the CFPB’s earned wage access specifications, DailyPay created the following EWA analysis rubric:

At the highest level, if there is no employee repayment obligation, it is not credit. If employee repayment is required, it goes into the very nuanced chart of compliance risks and rules. For example, the CFPB has said that if a provider is in fact requiring an employee pay back and that payback is done through a payroll deduction, it’s limited to 60% of the actual pay.

“That’s an incredibly onerous restriction for employers to ensure [compliance] with. Literally every week they’d have to have reporting, compliance, and auditing to ensure they’ve limited themselves to 60% because if they don’t, the vendor per this order is not going to be compliant with safe harbor,” said Lee.

The CFPB’s December 2020 follow-up order

On Dec. 30, 2020, the CFPB issued a follow-up order in response to its November advisory opinion. According to DailyPay, in the order “the CFPB indicated that earned wage access providers that leverage debiting as a form of payback cannot rely on a credit safe harbor, and are likely to be seen as making extensions of credit.”

In other words, employers partnering with EWA providers that debit could be at risk for legal and compliance challenges. “There’s a universal principle out there, which is if you give money to someone, don’t go into their bank account to take it back. Because that could cause all sorts of issues for overdraft,” noted Lee.

Even so, several EWA providers that integrate with employers still rely on debiting as a means of repayment. “The reason why this is such a rife practice is… it takes time and effort in partnership and technology to build a platform that does not have to rely on going into a bank account to take out the money,” he added.

The legality of wage deductions

Another method of repayment is payroll deduction. In the context of earned wage access, payroll deduction is a way for employees to repay for wages that were accessed in advance of payday. The practice is illegal in many states.

“When employers process payroll deductions, they have to be very mindful of whether or not that payroll deduction is going to constitute something called a prohibited or illegal wage deduction, which is the case in 14 states across the U.S. The less technical way of saying that is there are a bunch of rules out there that say employers cannot dock your pay for [reasons] other than standard deductions like taxes or garnishments,” said Lee.

Employers using the wage deduction method remain exposed to state wage and hour laws, which were excluded under the safe harbor, and are not covered for these risks under the November opinion or the December order. Further, core compliance, tax, and additional workflow implications caused by payroll deductions were not eliminated by the CFPB’s announcements.

What does that mean for employers?

EWA vendors getting a “no-credit safe harbor” for themselves can come at the expense of employer wage and hour compliance for wage deductions. Employers using wage deductions for on-demand pay transfers are at risk of violating wage and hour states, Department of Labor rules, and other rules and regulations. This is one of the key reasons DailyPay has warned about the use of this practice.

This makes it important for employers to consider what models their EWA vendor uses. “For employers who are looking at earned wage access when they’re considering a particular vendor provider for a solution, it really gets into the sophistication of the platform of that particular vendor. You need an organization that has the technical capabilities to be able to deliver solutions without relying on things like debiting,” said Grotta.

The takeaway

The CFPB’s advisory opinion and follow-up order were released to provide clarity on certain types of earned wage access that require an employee to repay paycheck advances. It indicated that programs that require an employee to pay back an on-demand transfer through a payroll deduction could be considered extensions of credit. Payback models, and in particular payroll deductions, continue to face legal prohibitions, compliance issues, and other workflow implications that put employers using them at risk.

These risks do not apply to non-payback models like the one DailyPay follows. To mitigate risk, employers looking to partner with an earned wage access vendor should seek out an organization that utilizes a non-payback model approach.