No wallet, smartphone or credit card needed. European customers will be able to enter a shop, choose what they want and pay without having any of the above with them.

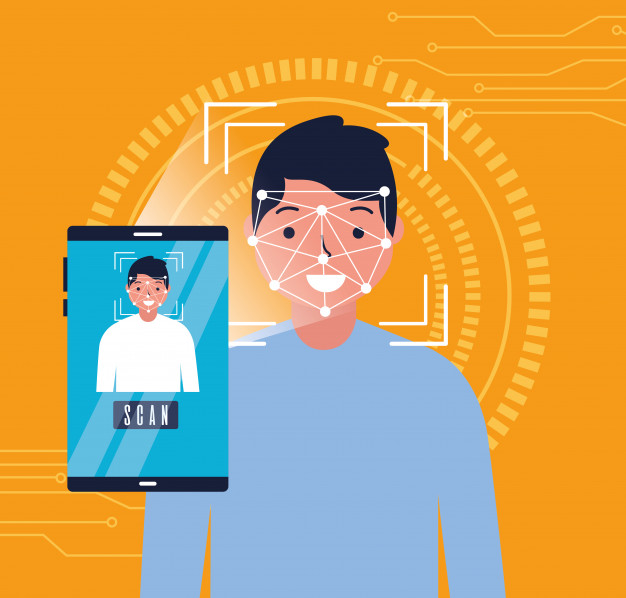

PeasyPay, a startup incorporated in Hungary, is letting people pay by just showing their faces and taking a picture of the palm of their hands, making the whole process faster and more convenient.

PeasyPay was launched by EIT Digital within its Innovation Factory, where a number of EIT Digital Partners come together to launch a deep tech venture into the market.

The project’s codename is “Pay with a Smile” and it is within the Digital Finance portfolio of the EIT Digital Innovation Factory. The partnership behind the initiative includes two Spanish partners, Ci3 and Liberbank, two Hungarian ones, E-Group and OTP Bank, and Slovenia’s AV Living Lab.

“The system is composed of three elements,” PeasyPay’s product leader Csaba Körmöczi explains, “a smartphone app for the customer (used only during registration), a smartphone app for the merchants, and the payment terminal”.

Digital profiles of the customers’ palms and faces are created through the app (available on both Android and iOS) by taking a selfie and a picture of their palm with their mobile’s camera. Afterwards, they have to register their bank card details on an integrated, secure payment gateway.

The actual in-store payment process is implemented by using a special point-of-sale (POS) machine, equipped with cameras and facial recognition software that scans customers’ faces and palms and compare them to the biometric template created in advance.

In the case of a match, the payment is authorised, and the amount charged to the credit card registered in the payment gateway of the corresponding PeasyPay account.

The combination of face and palm scanning solves the issue of mismatching a person, as facial recognition systems’ accuracy degree can vary significantly depending on the person, software and situation.

The PeasyPay solution has also been designed to be fully compliant with all European regulations, especially GDPR and national data protection laws. Under GDPR’s provisions, the processing of biometric data for uniquely identifying purposes is not authorized, unless the data subject has given explicit consent for a specified purpose.

Another factor that makes the startup’s technology stand out from the competition is thatother payment solutions are fully dependent on a proprietary infrastructure and ecosystem, whereas PeasyPay is based on an open system; any bank and any merchant can join.

The PeasyPay solution has been operational in Budapest since December 2019 – with a break in the spring due to the pandemic – in a coffee shop frequented by the tech-savvy employees of the city’s second district.

OTP Bank and e-Group are joining forces to spread PeasyPay further in the Hungarian capital: a marketing campaign will engage members of the local hospitality industry and retail sector.

A pilot use case of PeasyPay, targeting the city’s food, retail and hospitality industry, is currently ongoing in Guadalajara, Spain. The trial started in July, in four small shops located in the city centre, and is being extended to other businesses. In total, 25 proximity shops (bakeries, butcher’s shops, grocery stores, cafés, bookstores, print shops, and herbal shops) will be participating in the Spanish pilot. The plan is to make the PeasyPay solution available in department stores as well.

More pilots are planned elsewhere. In the UK, the system is being set up to let taxi drivers seamlessly pay the fee to enter Glasgow Airport’s parking area. In Slovenia, the pilot will take place in a restaurant.

During the pilot phase only customers based in Hungary, Spain, Slovenia and the UK will be able to download PeasyPay from their local app store. By the end of the year, the app will be rolled out globally.

About EIT Digital

EIT Digital is a leading European digital innovation and entrepreneurial education organisation supporting the creation of a strong digital Europe.

EIT Digital is focused on building and scaling ventures, and on breeding and up-skilling talents to equip them with both digital and entrepreneurial skills. It does this by mobilising a pan-European ecosystem of over 300 top European corporations, SMEs, start-ups, universities and research institutes. As a Knowledge and Innovation Community of the European Institute of Innovation and Technology, EIT Digital is focused on entrepreneurship and is at the forefront of integrating education, research and business by bringing together students, researchers, engineers, business developers and entrepreneurs. This is done in our pan-European network of Co-Location Centres in Berlin, Budapest, Eindhoven, Helsinki, London, Madrid, Paris, Stockholm and Trento. We also have a hub in Silicon Valley.

For more information, visit www.eitdigital.eu