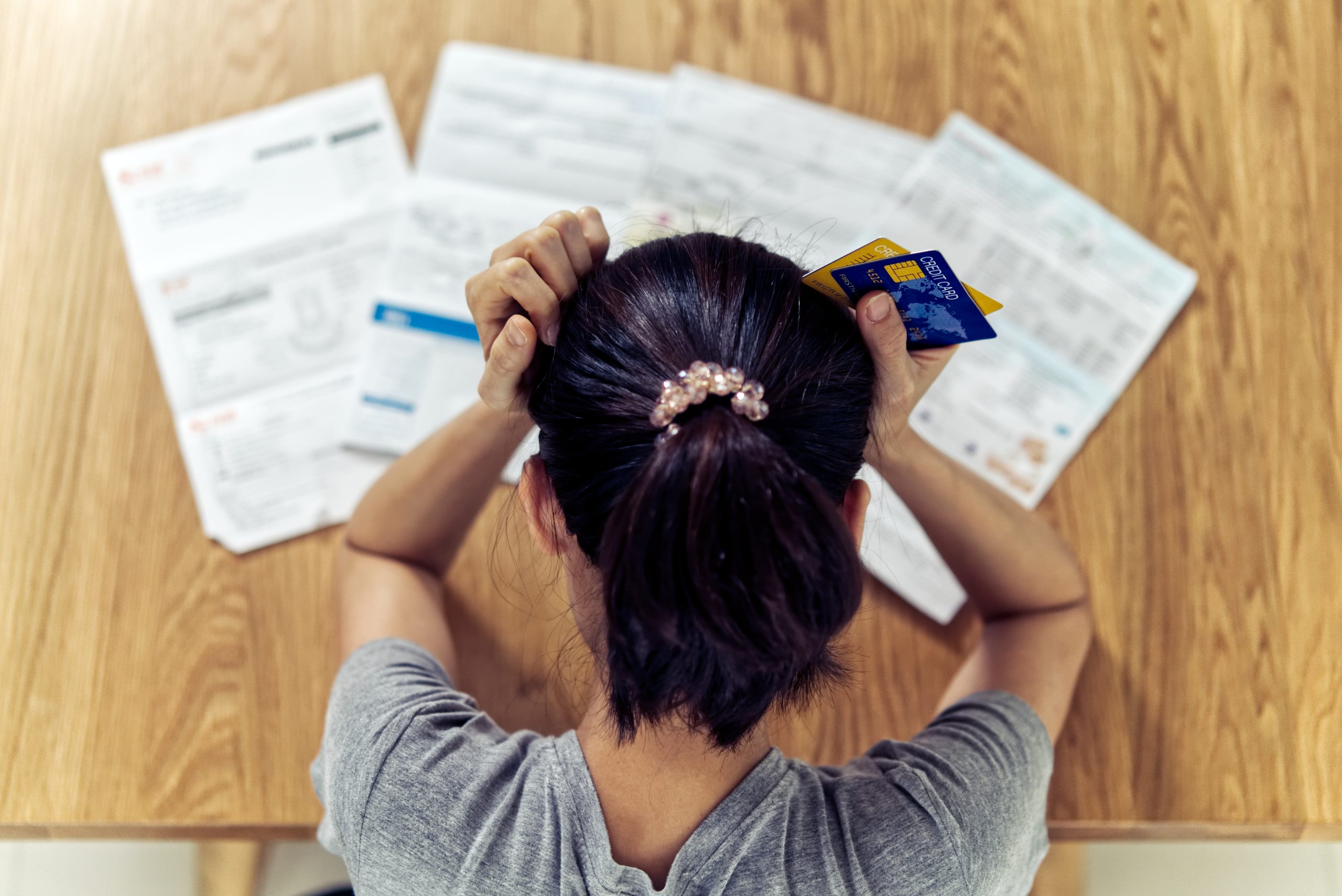

As interest rates continue to rise, many U.S. consumers are feeling the pressure of higher borrowing costs. For those already burdened with significant consumer debt, the impact of rising rates is particularly concerning, potentially leading to financial instability and difficulty managing monthly payments.

The Impact of Rising Interest Rates

Interest rates affect everything from credit card balances to mortgage payments. As rates increase, the cost of borrowing rises, leading to higher monthly payments and greater overall debt. For consumers with variable-rate loans or credit cards, the effects can be immediate, putting a strain on household budgets.

The Consumer Debt Burden in the U.S.

American consumers have been taking on more debt in recent years, driven by factors such as low-interest rates and easy access to credit. However, with rising rates, the cost of servicing this debt is becoming more challenging. High levels of credit card debt, auto loans, and student loans are particularly worrisome, as consumers may struggle to keep up with payments as interest costs climb.

Financial Risks and Challenges

The combination of rising rates and high debt levels poses several risks for U.S. consumers:

- Increased Financial Stress: Higher monthly payments can lead to increased financial stress, making it harder for consumers to manage their finances and potentially leading to missed payments or defaults.

- Reduced Spending Power: As more income is allocated toward debt payments, consumers may have less money to spend on other goods and services, potentially slowing down economic growth.

- Credit Risk: Consumers with high debt levels may face difficulties accessing additional credit or may see their credit scores decline if they struggle to keep up with payments.

What Can Consumers Do?

For debt-laden consumers, it’s important to take proactive steps to manage the impact of rising rates:

- Refinance Loans: Refinancing existing loans to secure a lower fixed interest rate can help reduce monthly payments and protect against future rate increases.

- Pay Down Debt: Prioritizing debt repayment, especially on high-interest loans, can help reduce the overall cost of borrowing and improve financial stability.

- Budget Wisely: Reviewing and adjusting household budgets to account for higher payments can help consumers stay on top of their finances and avoid falling behind.

The Road Ahead

As interest rates continue to rise, U.S. consumers will need to navigate the challenges of higher borrowing costs carefully. Those with significant consumer debt burdens must be especially vigilant in managing their finances to avoid the pitfalls of rising rates.

Rising rates are triggering alarm bells for debt-laden U.S. consumers, underscoring the importance of proactive financial management in an increasingly challenging economic environment.