As the economy becomes increasingly global, businesses are sending and receiving payments to and from a multitude of countries. This has resulted in a significant increase in cross-border payments in recent years, and this trend will only continue to rise. Yet, cross-border payments still rely on inefficient legacy processes and methods, and thus, are an area ripe for innovation.

Since cross-border payments can often be unpredictable and costly, businesses that operate globally need to implement solutions that enable seamless, secure, and fast global transactions. To share best practices and strategies on how this can be done, Wells Fargo recently issued a white paper on effective and innovative cross-border payment strategies.

Dealing With Growth and Complication

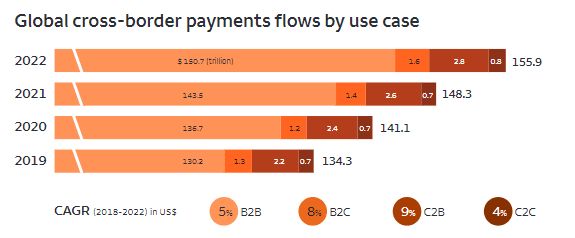

Cross-border payments are on a significant growth trajectory. The white paper noted that businesses processed approximately $145 trillion in cross-border transaction value in 2021, which represents a compounded annual growth rate (CAGR) of 5% since 2018.

Business-to-business (B2B) payments make up the overwhelming majority of cross-border payments, as seen in the chart below based on data from Ernst & Young Global Limited.

Cross-border payments can be a multistep, costly process rife with friction. They involve a sender initiating a cross-border payment transaction through their bank, the originating bank. The sender’s bank then makes the payment using correspondent banks and/or financial market infrastructures (FMIs). Finally, the beneficiary bank (the recipient of the payment’s agent) receives and processes the payment, finally making money available to the recipient.

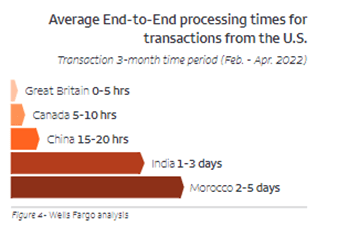

“Processing time can vary greatly between the in-flight intermediary leg and the beneficiary leg,” said Joanne-Strobel-Cort, Head of CIB Segment Solutions Advisory, Global Treasury Management at Wells Fargo. “Processing time is dependent upon several factors including the number of banks, banking transfers, or entities required to get the payment to its final destination. Friction in cross-border money movement can occur at any point, and is often the result of bank or region-specific informational requirements.”

The process can often vary depending on whether it involves book or off-book transfers. Book transfers are those where there are common banks on both sides of the transaction. Off-book transfers are those where the sender and receiver have accounts at different banks.

As a result, there is a great deal of variability in the steps required and the time it takes for payments to reach the beneficiary. The largest friction point often relates to the information required by the intermediary bank and receiving bank to process the payment. Depending on which country the payment is going to, cross-border payments can take up to several days to settle.

Processing Challenges Associated with International Money Movement

Several challenges in the process prevent the seamless and predictable processing of cross-border money movement.

One is predictability. As noted in the section above, there can be multiple touch points in the process; payments don’t simply go from point A to point B. Then, there is the cost involved. Several banks, clearing market infrastructures, and payment service providers may be involved in processing cross-border transactions, and each one may generate a fee. The white paper noted that the average cost to complete a cross-border payment can range anywhere from 6.5% to 11% of the total transaction amount, a stunningly high figure.

Different country-specific requirements can also play a big role in creating friction in international money movement. In some countries, incoming payments can’t settle unless a human is on the other end of the transaction manually approving a payment before it is credited to a recipient’s account. When significant time zone differences are involved, this requirement for human involvement can also lead to delays.

International money transfers also typically have a longer processing chain compared with domestic transfers, given the need for more rigorous screening.

“If proper documentation is not received or the transmission of payment information is not fully passed through each correspondent bank payment processor, market infrastructure, or beneficiary’s bank, the transaction can be sent back,” Ms. Strobel-Cort stated. “We are looking for the industry move to the ISO 20022 format to vastly improve the structured movement of information between participants and market infrastructures in cross border payments. Additionally, SWIFT’s new Transaction Management Platform should improve immutability of information in specific fields as information passes between participants of the cross-border payment ecosystem,” adds Strobel-Cort. She further explains that “In addition to validating the necessary information, cross-border transactions typically undergo a sanctions screening within the originating country (as well as the beneficiary country and any intermediary agent country in between) to comply with sanctions laws, which may also add friction.”

Strategies for Streamlining Cross-Border Payments

Luckily, there are strategies companies can put into place to make the process more frictionless and predictable.

First, businesses should always provide full information for both originators and beneficiaries; this includes full street address, full names, and complete city, state/province, country, and postal code, along with any required identifiers such as a passport number for government identification.

It’s also important to embed prepayment tracking analysis and validation to ensure as smooth a process as possible. This includes validating all information about the receiving party — especially if it is a new receiver — and validating all payment information before the transaction is initiated. Companies should also work with a processor or bank that provides the ability to track and monitor the transaction throughout the transaction process to ensure there is reporting in place if a transaction fails midstream, the white paper stated.

Additionally, businesses should explore the use of artificial intelligence (AI) to identify and automate repetitive processes. Machine learning can enable automated, rules-based, repetitive payments, allowing predictable transactions to be executed with a minimum number of processing steps. Also, if there are regular problems with certain types of transactions, AI tools can automate them, so the same issue doesn’t occur each time.

Finally, it’s important to find a partner that can fill more specific needs than can be done with internal resources. The white paper noted some examples:

- Data translation firms that can turn data and transform them to the receiver.

- Data security firms that are highly skilled at helping prevent fraud and keeping data secure across borders.

- Data or fintech firms that can make data actionable by transforming them into a usable format for cross-border transactions.

Conclusion: The Continued Growth of Cross-Border Payments

As noted, cross-border money movement shows no sign of decelerating, so this will only become a bigger issue for companies in all geographies. As such, large banks, payment processors, associations, governments, and fintechs are all racing to meet heightened expectations for money movement.

The winners will be companies that recognize the opportunity to simplify their processes and are eager to drive innovation for themselves and their global business partners. With the proper rigor, partnerships, and investments in automation, businesses can make cross-border money movement more predictable, seamless, and timely.