Banks and fintechs rely on each other in many ways, but this hasn’t stopped both sides from jockeying for top-of-wallet status.

At the heart of this complex relationship is data. As the open banking model has proliferated, banks have shared customer-permissioned data with third-party providers in exchange for a range of digital services that were previously not possible with traditional systems.

While this may have initially shifted the balance of power in fintechs’ favor, financial institutions have begun to reestablish themselves. As Matthew Gaughan, Payments Analyst at Javelin Strategy & Research, detailed in the Monetizing the API: Banks Are Increasingly Generating Funds from Tech report, this inflection point has been driven in part by payment APIs.

Within open banking infrastructure, banks now have the capability to leverage these APIs to drive higher transaction volumes and identify cross-selling opportunities, unlocking revenue for those that optimize them.

Approaching the API Strategy

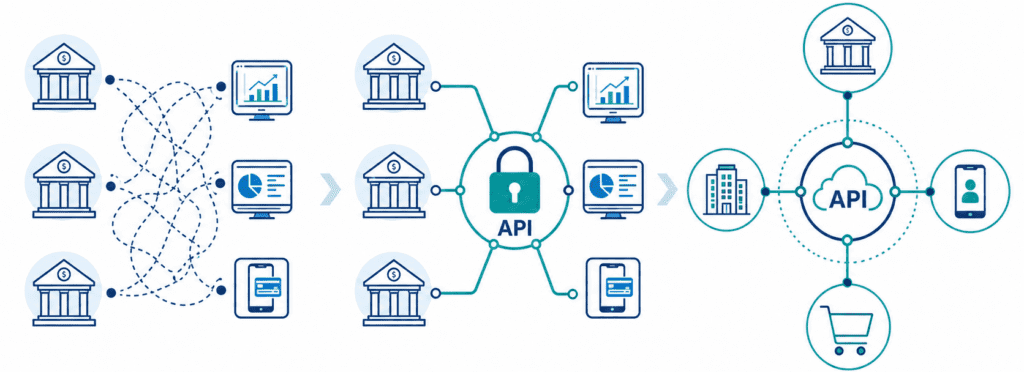

When leading financial data aggregators like Plaid and MX first came to market, screen scraping was the only way to access consumers’ financial data. While this technique gave third parties access to account-level data and potentially transaction-level data, it also created security risks.

These risks initially raised concerns on the part of banks, but the benefits of fintech services often outweighed them. Through these partnerships, banks could leverage financial technology to achieve higher transaction volumes, improved authorization rates, and lower cost of funds.

However, the screen scraping model gradually faded as open banking APIs emerged. Not only did payment APIs provide a more secure connection, but they were also more efficient and cost-effective.

This shift spurred the development of an API layer that now serves as critical infrastructure for the global financial services ecosystem.

“Just viewing it that way made it much more of an efficient relationship and that brought new benefits to FI’s and gave them insight into how they could maybe utilize this more internally and more on a proprietary level,” Gaughan said. “Some of the fintechs that utilize Plaid or any of these companies were initially strong guides for how banks approach their API strategy.”

Two-Part Monetization

Following the proliferation of payment APIs, many leading U.S. banks launched developer portals. These platforms allowed fintech companies like Plaid and Stripe to securely connect to financial institution’s systems.

This dramatically expanded opportunities for fintechs to distribute their products, but it also created benefits for banks.

“For banks, you saw the same thing. Their payment and banking products can now be more widely distributed to third-party developers and applications,” Gaughan said. “You’re getting this two-part indirect and direct monetization where indirectly they’re benefiting from those many-to-many connections through those financial data intermediaries.”

This revenue generation became possible because banks invested in developer portals and proprietary APIs for their financial products, which in turn drove higher transaction and payments processing volumes.

Over the past few years, these institutions have further embedded APIs into their tech stacks, continuing to unlock new revenue streams.

“It is combining their expertise and offering industry specific and modular API product suites that can be embedded into a company’s existing framework,” Gaughan said. “An example of that is what JPMorgan is doing for marketplace clients like Walmart, providing different payments capabilities—whether it’s money movement, payouts, acceptance, or onboarding—through a single embedded finance API.”

“Not only does this create new cross-sell opportunities and strengthen existing relationships, but it also drives revenue in some of the previous iterations of the evolution,” he said.

Tipping in Banks’ Favor

With this evolution, there has been a corresponding realignment in how data is governed and managed. However, this new model has also raised important concerns.

For example, there is ongoing industry speculation about which party is ultimately responsible for consumer-permissioned financial data once it is shared. There are also questions about regulatory actions that could emerge.

Despite these uncertainties, the evolution of payment APIs has provided a much-needed reset for banks. When fintech intermediaries first emerged, many banks didn’t fully understand the implications of opening transaction and account data to third parties.

Now that banks have a clearer understanding of the landscape, many are pushing for change. For example, JPMorgan Chase shifted the dynamic when it announced it would begin charging fintechs for data access that they previously provided for free.

This realignment has created some tension between banks and fintechs, and it is unlikely to be the last time these partnerships evolve. Still, the ongoing synergy between the two sides suggests that periodic disagreements are unlikely to escalate into a full-scale rift.

“There’s always going to be a codependence that remains between financial institutions and those intermediaries,” Gaughan said. “But it just would be too much money and too labor intensive for banks to try to recreate the many-to-many scale that your Plaids and MXs provide.”

“But with having their own developer port or proprietary APIs and embedded finance solutions and where they’re going more in direction where they’re using that data to their advantage, you’re seeing the leverage tip more in banks’ favor again,” he said.

A Premium on Expertise

Another reason banks are taking the lead is the growing complexity of open banking, where emerging products are underpinned by regulated, customer-permissioned data.

“Banks have an advantage there because they could manage these new revenue streams and the risk and compliance associated with that, and any other payment business it operates,” Gaughan said.

“It’s crucial that they have a structure in place to handle the different reporting requirements,” he said. “They’ll have audits from different regulators; they’ll need to make sure they’re up to snuff on their risk mitigation techniques and make sure they are protecting those consumer funds and limiting the bank’s exposure.”

Fortunately for banks, many of which have managed compliance and risk obligations for decades, these are areas where they often have deep institutional strength.

“They’re strong and they’re positioned to benefit because what you’ll see, especially now with agentic commerce and AI. There’s going to be a premium put on the risk and compliance expertise,” Gaughan said. “Ultimately, that’s a signal to merchants and fintechs that are looking to accept and process payments, a signal that banks are still a safe place to do so.”