Beyond accelerating settlement and clearing times or giving merchants a pathway to better liquidity, real-time payments hold transformative power on a global scale. According to ACI Worldwide’s Real-Time Payments: Economic Impact and Financial Inclusion report, real-time payments are bringing millions of people into the financial ecosystem, opening new markets for financial institutions, and bringing lower costs and higher efficiency to consumers, businesses, and governments.

Published in collaboration with the Centre for Economic and Business Research, the report demonstrates—for the first time—an empirical link between real-time payments and financial inclusion and the associated enhancements in financial security, entrepreneurship, digital transformation, and the expansion of banking services that financial inclusion brings.

As the report’s introduction notes, “Real-time payments are a win-win proposition for all stakeholders in the world’s payments ecosystem.”

‘At Every Level of Society’

The study focused on 40 countries, reviewing historical banking data and applying a predictive model. Among the findings and projections:

- Real-time payments in 2023 boosted the gross domestic product across all 40 countries by $164 billion (or the equivalent of the labor output of 12 million workers).

- By 2028, the GDP contributions from real-time payments will reach $285.8 billion, a 74% increase from 2023.

Real-time payments—whereby payers and payees can complete their business in seconds through digital tools rather than waiting for days with legacy methods—fuel economic growth “at every level of society,” the report notes, and create market efficiencies in the economies they touch.

The report also examines specific developments and opportunities in various regions: Africa, Asia Pacific, Europe, Latin America, Middle East, and North America.

The driving factors vary—in Africa, a youthful population is enjoying robust real-time payment ecosystems, while North America is seeing more incremental growth—but a larger story is emerging across the globe: Real-time payments are transforming economies and creating opportunities for businesses and consumers.

A Matter of Inclusion

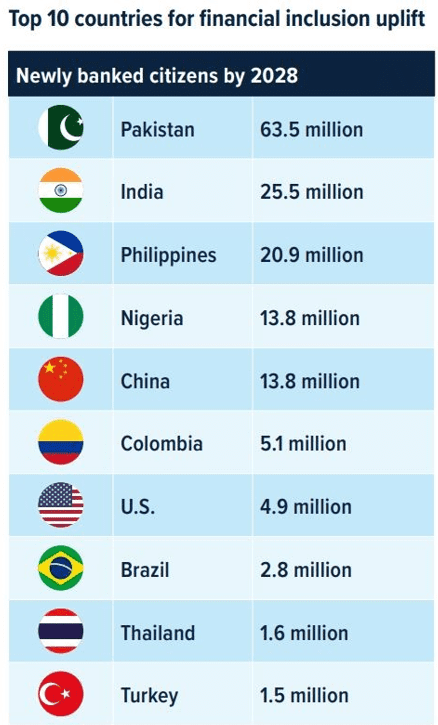

The report takes a deep dive into financial inclusion, studying data from 28 countries to chart the link between real-time payments and the expanding reach of financial services. By 2028, more than 167 million people previously excluded from the financial system could have bank accounts. The 10 countries poised to see the most uplift into financial inclusion are a mix of nascent and mature economies. Pakistan is number one (with an estimated 63.5 million people newly banked by 2028), and Turkey is number 10 (1.5 million), with economic powerhouses like China (13.8 million) and the United States (4.9 million) at numbers five and seven, respectively.

Although the inclusionary effects of real-time payments are profound in rapidly developing economies—much attention has been granted to the rise of such payments in India, for example—the reach is more egalitarian. Those historically left behind even in advanced economies can be allowed to leverage more affordable and accessible financial services through real-time payments and subsequently avoid predatory fees and loans.

Real-time payments can eliminate the barriers caused by fees and delays in payment timing and reduce the late fees that often occur amid payment lags. This means that apps, QR codes, and mobile wallets can be the portals for previously unbanked and underbanked citizens to access products that could transform their lives.

Fees have a particular impact on unbanked or underbanked populations. For example, a recent U.S. Consumer Financial Protection Bureau report on overdraft and non-sufficient funds fees found that the median fee amount was $35. Roughly half of consumers in the CFPB study were not prepared for the overdraft fee, and those who incurred fees were more likely to come from lower-income households. In addition, lower-income households are more likely to experience income volatility or live paycheck to paycheck. This makes certainty about the timing and availability of funds even more critical.

“In some areas, the barrier to becoming banked has likely been cost,” said Elisa Tavilla, Director of Debit Advisory Services at Javelin Strategy & Research. “You usually have to maintain a minimum balance in the account or pay maintenance fees. Maybe they weren’t in proximity to physical branches, which used to be the primary way to access banking services. Now, with digital and mobile, banking is a lot more accessible no matter where you are.”

The Financial Uplift for Merchants and Banks

The dramatic effects of real-time payments go far beyond consumers. Merchants also experience reduced transaction fees—or none at all—when they accept real-time payments. Receiving funds in seconds rather than days can be crucial for businesses that rely on daily cash flow. Instant settlement also helps merchants keep better tabs on their inventory and reduce their overhead.

The ACI Worldwide report indicated that real-time payments generated $116.9 billion in savings for consumers and businesses in 2023, mainly due to lower transaction fees and reduced settlement float times. These savings are predicted to grow to $245.8 billion by 2028.

The effects of real-time payments can also be seen in the most basic marketplace meetings. Tavilla noted that she had recently been in Thailand (No. 9 on ACI Worldwide’s list of the top markets for financial inclusion uplift) and saw that “street vendors who used to accept only cash now have a QR code posted.”

“When the money gets deducted directly from a bank account, the merchant immediately knows they’re getting paid,” she said. “It’s just convenient, and everybody seems accustomed to using it.”

These remarkable efficiencies—coupled with the surge in financial inclusion—present significant opportunities for banks. The report identifies the top markets for increased profit opportunities by 2028 through accountholder growth aided by real-time rails. Again, Pakistan takes the top spot ($173 billion), followed by Argentina ($3.4 billion), with major economies like India, China ($21.2 billion), the United States ($18.9 billion), and Brazil ($8.9 billion) also in the top 10.

That influx of newly banked citizens brings opportunities to build new products and services and grow new generations of customers.

As the report notes, “Real-time payments have asserted their role as a powerful enabler for societal transformation.”

*All data contained within this article comes from the Real-Time Payments: Economic Impact and Financial Inclusion Report