Financial institutions are among the most trusted entities in the world. Consumers believe their banks act in their best interests—especially when it comes to protecting them from fraud. They expect strong, effective solutions that support their everyday financial activities, safeguard their accounts, and secure their identities.

But trust isn’t automatic—it must be earned. Nowhere is this more true than in the fraud dispute process. In a PaymentsJournal Podcast, Ryan Sorrels, CRO at Quavo, and Suzanne Sando, Lead Analyst of Fraud Management at Javelin Strategy & Research, discussed how, instead of letting disputes drive customers away, banks can use these moments to build deeper trust and strengthen relationships.

Restoring Confidence After Fraud

There is a lot of room for improvement within the fraud dispute process. According to Javelin, nearly half of fraud victims wished their financial institution had treated them like a victim—not a burden.

Banks need to refocus on ensuring that this difficult experience doesn’t lead to further negativity. In fact, many customers say the way a bank handles the resolution process has a greater impact on their trust in the institution than the fraud itself.

“They’re already having a negative experience of fraud,” said Sorrels. “We don’t want to compound that with another negative experience. Let’s take that negative experience and show up to give a great experience. You’re doing a tremendous amount to reinforce loyalty as opposed to compounding the problem and eroding loyalty even further.”

Many fraud victims want better tracking throughout the claims and dispute process. A small subset of bank consumers file fraud disputes and then never receive any follow-up. This could be due to a lack of standardized and automated procedures to make the dispute process more efficient. Some of these cases might be falling through the cracks, leaving customers feeling like they’re not a priority. Ultimately, that would make anyone feel unhappy with an organization they do business with.

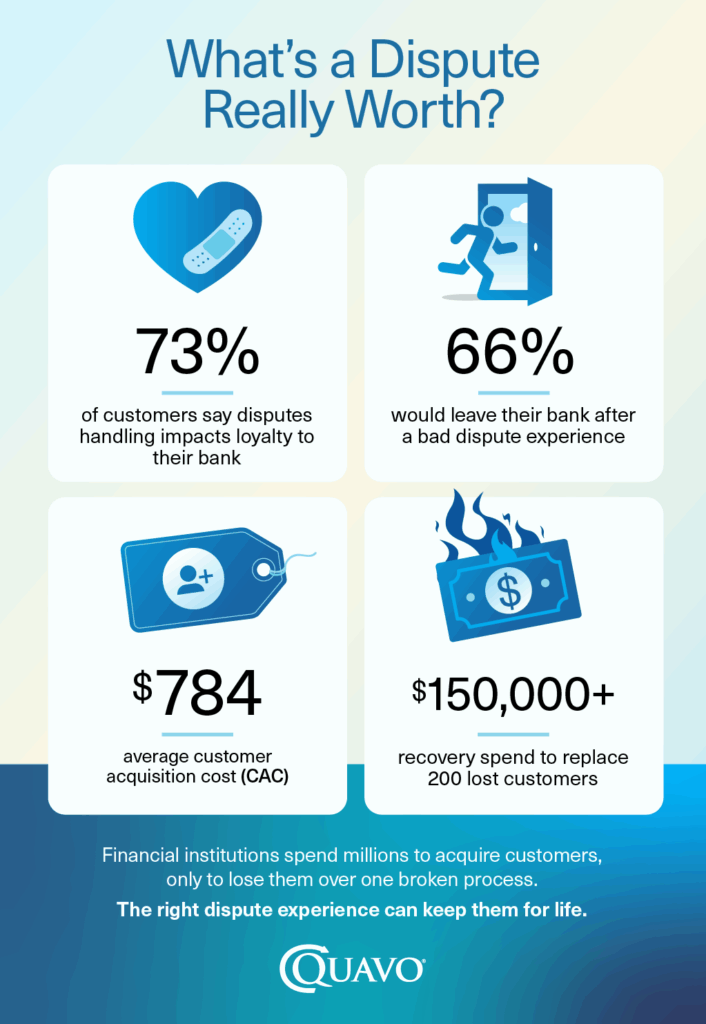

The Customer Cost

Historically, the dispute resolution process has been viewed as a back-office function—primarily focused on cost, efficiency, and staffing requirements. What’s been less examined is the economic impact on the customer experience.

When banks deliver a strong dispute experience, they build trust and enhance loyalty. But a poor experience can have the opposite effect, driving customers away. In fact, many customers say the way their bank handles fraud disputes influences their loyalty—and some are even willing to switch banks after a negative experience.

“We’re so interconnected with our accounts, so it’s a lot of work to go through the process of closing an account, opening a new one and getting everything set back up,” said Sando. “There’s a lot of rigamarole around closing those accounts, reopening somewhere else, reestablishing all those connections, making sure your information is correct. If fraud victims are willing to go that extra mile, that speaks volumes to the importance of making sure that the customer experience is prioritized, and that you’re focusing on reducing that unnecessary friction and maintaining that loyalty and trust.”

Banks invest millions of dollars in customer acquisition, with the average cost exceeding $700 per customer. Maybe only 10% of people presenting disputes have a negative experience, but two-thirds of those are at risk of leaving. The cost to reacquire those customers can add up quickly. Even if just 200 customers ultimately leave due to a negative experience, that’s nearly $150,000 just in customer acquisition costs alone.

Customers who don’t leave risk moving the bank to the back of their wallet. They may stay, but they might adopting fewer products or use existing ones less frequently.

Eliminating Friction with AI

Much of the friction in today’s dispute process stems from outdated, inefficient systems. But with the right tools and automation in place, that can change drastically, and that’s exactly where Quavo is leading the charge.

Take the intake process, for example: on average, it takes a customer around 10 minutes to file a dispute. With Quavo’s AI-driven platform, that time drops to just two minutes.

But it’s not just about streamlining intake, it’s also about accelerating resolution. Accountholders don’t want to wait days or weeks for answers. These are emotionally charged moments, and every delay compounds the stress. Customers expect responsiveness and swift, fair outcomes.

Speed alone, however, isn’t enough. Transparency is equally critical. When accountholders are at their most vulnerable, they need to know their claim is being investigated, and that their financial institution is keeping them informed every step of the way.

With Quavo, issuers can deliver a faster, more transparent, and empathetic experience, end-to-end, through the digital channels customers already rely on, such as mobile and online banking.

Managing Expectations

Fraud victims want a realistic timeline for resolution that aligns with the nature of their dispute. It’s entirely reasonable for them to want to know what to expect. By setting clear expectations, banks can turn a negative, stressful situation into a more manageable—and even positive—experience for the customer.

Customers are more cooperative when they know what to expect and when to expect it, whether the situation is stressful or routine. Financial institutions need to keep customers informed throughout the dispute process: when their participation is needed, what updates they can expect, and how the process works.

“I don’t think that’s a lot to ask for when you’re working through a process that isn’t standardized or is very much dependent on the employee that you as a customer happen to be working with,” said Sando. “Things tend to be dealt with on a case-by-case basis, and that introduces inconsistency, uncertainty, unnecessary friction into an already stressful situation.”

Certain cases, like first-party fraud, require more manual review and a personalized approach. However, in general, an unstandardized process accountholders valuable time—time that could be better spent on higher-priority, customer-facing matters.

The Advantages of Automation

There are solutions that can automate much of this process behind the scenes. When employees trust that these tasks are being handled efficiently, they can spend more time on special cases. This allows employees to devote more attention to customers who need it, making them feel like a priority.

Maintaining and growing brand loyalty and trust with the bank also involves improving these high-stress situations. It ultimately comes down to customer sentiment. At the end of the day, do they feel like they were treated as a priority? Do they have a satisfactory experience where they can say their bank handled the situation well and feel even better about the relationship going forward?

“Trust is the center of the customer bank relationship,” said Sorrels. “When there’s fraud on a customer’s account and a dispute process, it’s the banks opportunity to show up and create a great experience. On the flip side, if it’s a negative experience, it can really break that trust. The most important aspect to customer loyalty is: what are you doing with that customer’s trust?”