In light of the COVID-19 pandemic, technology continues to be a key pillar of our industry as we continue to serve our customers and communities. Now, more than ever, digital offerings are an important component to a comprehensive payment strategy.

Traditional financial institutions are also taking note of the sleek apps and intuitive user interfaces offered by big tech companies like Google, Apple and Facebook entering the payments industry and are beefing up their own digital offerings accordingly.

As customers migrate to digital services, mobile wallet usage has been on the rise and financial institutions are shifting their focus as a result. To learn more about the rise of mobile wallets and how community banks can offer their own mobile wallets, PaymentsJournal sat down with Tina Giorgio, president and CEO of ICBA Bancard, and Peter Reville, director of Primary Research Services at Mercator Advisory Group.

After some delay, mobile wallet use is on the rise

When companies first began offering mobile wallets in the early 2010s, pundits heralded the technology as the next big thing. But each year, despite the optimism, mobile wallets never saw widespread, sustained adoption.

Reville, who has worked with mobile wallets since 2011, explained that consumers were slow to adopt the technology for two major reasons. First, consumers did not “see the value in using their phone to pay for things over just taking their card out of their wallet.” Part of this reservation stemmed from the fact that people already trusted their traditional financial products and the institutions that offered them.

Any new financial product is met with some degree of skepticism until it becomes more familiar. “People need to understand the technology, understand what it does, and then develop a trust that their money is safe when they use this technology,” noted Reville.

The other barrier to adoption was that mobile wallets could not be used in the majority of stores. “Despite the move to EMV, where many retailers decided to also enable NFC, there was spotty coverage for mobile payments.” However, despite a slow start, mobile wallet adoption is poised to take off.

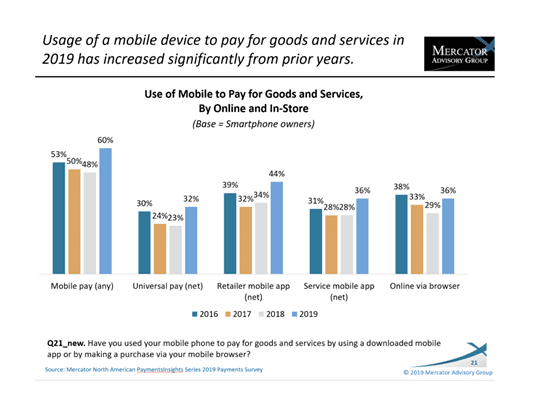

“Times are changing,” said Reville, “comfort levels are increasing, more portfolios are being opened up to mobile wallets, and the number of terminals which accept mobile payments is increasing.” According to data from Mercator Advisory Group, the use of mobile applications to pay for goods and services has risen notably over the past year.

In 2018, for example, 48 percent of respondents reported using mobile pay; in 2019, this number surged to 60 percent. “And I would expect that these numbers are going to continue to increase,” predicted Reville.

Community Banks should adopt mobile wallets

Based on the growth of mobile wallet use, Giorgio recommended that community banks take notice of the trend and offer their own mobile wallets. Banks that have done so have seen positive results.

“ICBA Bancard had a big push a couple of years ago to enable wallets for all of our clients and we have seen pretty good results there,” explained Giorgio. “What we’re driving for is a payments app on every community bank customer’s phone that becomes the wallet of choice for all things payments.”

Both Giorgio and Reville agreed that community banks were well positioned to offer such a payments app because they enjoy the trust of their customers in a way that large tech companies do not. Tech companies have been struggling with data breaches and questions about data privacy, causing many consumers to regard these companies with a level of skepticism.

In contrast, “community banks are always a trusted source for their customers and their communities,” explained Giorgio. “So anytime that we can deliver features, functions, and capabilities that are on par with the device manufacturers, I think that there’s a tremendous opportunity to shift market share.”

Mobile wallets need to offer the right features and user experience

For banks to successfully offer mobile wallets, they need to provide a user experience and key features that consumers have come to expect from their financial apps.

“Whether it’s provisioning the card into the wallet in a seamless fashion, managing my spending, tracking my transactions, or managing my alerts, I think that that’s all expected today from a client perspective,” said Giorgio.

While creating financial apps brimming with functionality, it’s important that the apps remain easy to use. If there are too many useless features, or if the features are hard to understand, consumers may not want to use the apps. This is a problem that Ondot, a leading mobile payment service provider, identified in a previous PaymentsJournal podcast.

Giorgio recommended that in determining what features to include in an app, banks should consider what their customers actually want and offer that. Moreover, these features should be provided in the way consumers want.

ICBA Bancard is partnering with Ondot

In order to provide the best solutions to its community bank clients, ICBA Bancard partnered with Ondot. Ondot was a natural choice, as the company released their Card App solution last year. Prior to that solution, Ondot had been a card controls company, offering features to turn cards on and off, among other card control functionality. But with its Card App solution, Ondot has “basically taken their card controls solution and put it on steroids,” said Giorgio.

Through the partnership, ICBA Bancard’s clients can access Ondot’s Card App and white label it, meaning that the app will carry that community bank’s name and logo. The app provides users with card controls, spending insights—allowing users to track their spending by categories—card-on-file management, and the ability to make mobile transactions, online and in stores. It also facilitates the digital provisioning of a card directly into the wallet.

Helping community banks create a digital payment strategy

One of ICBA Bancard’s goals is to help community banks stay competitive in the increasingly digital world of payments. This is one of the reasons why ICBA Bancard partnered with Ondot to provide mobile wallet functionality. As Giorgio put it: “Mobile wallets are part of a digital payment strategy for any bank, especially community banks.”

To further aid community banks, ICBA Bancard is building guides and tools to help its banks develop their own digital strategies. “In 2019, we launched a consumer strategy tool that our banks can go to and interactively enter information about their banks’ products and services, and it will tell them where they are in their payments maturity model compared to other banks,” said Giorgio. This will help banks determine which areas they need to focus on to close the gap between them and their competitors.

Whether it’s through the partnership with Ondot or through creating educational resources and tools, ICBA Bancard is helping its community banks prepare for the future of payments.