Wire and ACH payments are an integral part of a financial institution’s strategy. With the introduction of The Clearing House RTP® service and the Federal Reserve’s plan to offer instant payments in 2023, organizations need to work out how these payment rails coexist and develop a roadmap that allows them to meet market demands. Meanwhile, the ISO 20022 standard will soon dominate high-value payment systems in the United States. What does this mean for high-value wire payments, which are critical and foundational to large corporate banks and financial institutions?

To learn more about how financial institutions can be ready for the next round of innovation, PaymentsJournal sat down with Kevin Peck, Director of Product Management for Enterprise Payments Platform at Fiserv, and Steve Murphy, Director of Commercial and Enterprise Payments Advisory Service at Mercator Advisory Group.

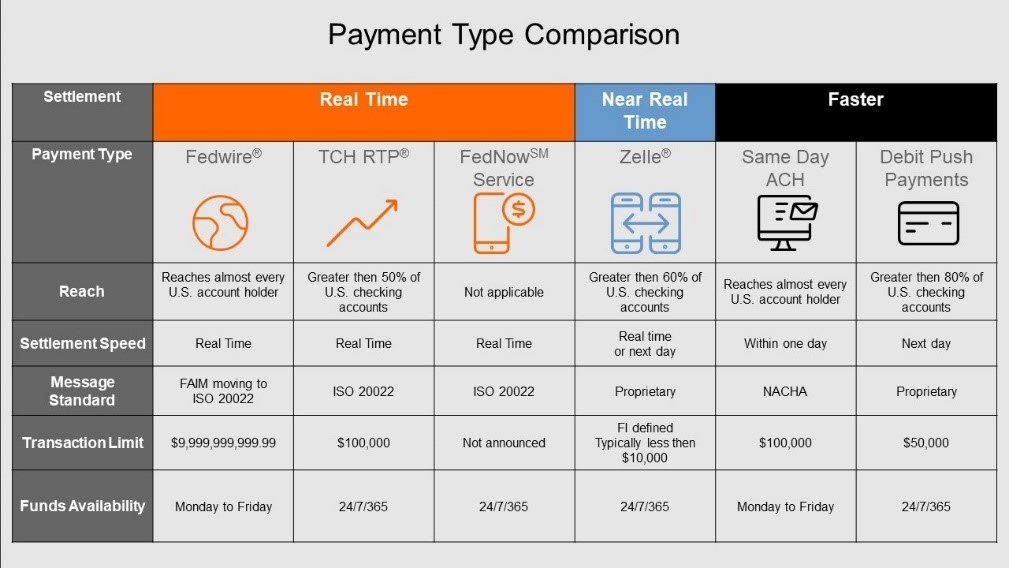

Breaking down payment types in the U.S.

It is important to understand the different types of payments in the United States and recognize the value they provide. According to Peck, there are three main payment types: real-time or instant payments; high-volume, low-value ACH payments; and high-value payments that are mostly corporate and interbank focused.

Payment types can be further broken down by features such as settlement time and speed, messaging standard, transaction limit, and funds availability, as shown in the chart below, provided by Fiserv:

Fedwire®, The Clearing House’s RTP network, and the upcoming FedNow service, all settle in real time, and use or will use the ISO 20022 messaging standard. A key difference between high-value wire payments and real-time payments is the amount of money that can be moved or settled in a single transaction. Currently, The Clearing House’s RTP network has a transaction limit of $100,000. In comparison, wire payments can move billions of dollars in a single transaction.

“The expectation on the real-time payments and eventually FedNow and even same day ACH is that the transaction limits are going to increase over the $100,000 limit that currently exists, which is going to spur additional B2B payments use cases,” explained Murphy.

Peck agreed, adding that “as it stands right now, the two main limitations [are] that transactions limit up to $100k for real-time payments as well as the ubiquity, so it doesn’t necessarily have access to every account in the United States.

Until the limitations surrounding real time payments networks are removed, wire payments will continue to dominate corporate use cases.

Even with the entrance of real time payments, wires remain relevant to financial institutions

Wires are a critical part of a financial institution’s payments infrastructure and revenue streams and contribute significant fee income. Effective use of Wire systems helps corporate treasurers’ cash management, improves transaction efficiency and reduces fraud.

“Listeners may not realize the extent to which wires underpin transaction banking revenue. They’re utilized in a wide variety of transactional use cases, and there’s literally trillions of dollars of value exchange that moves along these rails every day,” said Murphy.

Wires are a key utility for cross-border corporate payments, with capabilities such as the international movement of funds and executing FX transactions, providing banks with the opportunity to add value-add services that drive revenue.

“Wires are also used for bank reserve account requirements, Fed funds, repurchase agreements, trading account obligations, corporate client deposits, and all sorts of liquidity needs and payroll… so they are really the predominant choice for initiating cross-border payments,” Murphy added.

ISO 20022 will soon be the universal standard for wires

The shift to ISO 20022 is on the horizon for wire payments. ISO 20022 is a global messaging standard set by the International Organization for Standardization (ISO) that can be used for all types of financial communication.

ISO 20022 is rapidly becoming the universal standard for wire transactions, comes with enhanced remittance data information that far exceeds the capabilities of SWIFT. It is already used by payment systems in over 70 countries.

“What ISO 20022 is bringing [is] a much richer data scheme and [more] structured information into the processing that’s going to have benefits for financial institutions as well as their customers,” said Peck.

Financial institutions will benefit from access to better and more structured data, which makes scanning for sanctions and fraud easier and more robust, and drives down exceptions resulting in reduced operations costs. Customers will benefit from improved reconciliation and easier management of payments.

“The really big benefit across both financial institutions and customers is all that extra information that’s coming in. Being able to take rich data analytics and layer it on top as a value-added service to really drive better insights into those payments – how that money is moving, who you’re doing business with, and open up new opportunities to go after,” added Peck.

How financial institutions can prepare for ISO 20022

The ISO 20022 deadline is fast approaching. SWIFT is undergoing modernization efforts to move to ISO 20022 with a targeted adoption date of November 2022. Fedwire is also committed to ISO 20022 conversion, but has not announced a firm date which means they will not achieve full migration until the end of 2023 or later. Even so, the Federal Reserve will soon require all Fedwire transactions to have the capability to transfer the ISO 20022 information to enable coexistence with other clearing infrastructures that have already adopted to format. Meanwhile, CHIPS is aiming for full ISO conversion by November 2023.

“Changes are now coming down the pipe that banks are going to have to start expecting and planning for… All of these changes with the Fed and modernization of ISO 20022 [are] going to have a large impact on a financial institution’s back office,” explained Peck.

The path to modernization can be challenging, and most banks will find that they need to make significant changes to multiple systems to achieve ISO 20022 migration. From payment processing systems to accounting, the shift to ISO will have an organization-wide impact.

“The key [to modernization] is that banks and credit unions are looking for that partner, that flexibility, to be able to help them meet their needs. And that’s really what we focus on, is helping address [those needs] based on key drivers… and bringing the appropriate solution to the table to help them realize the strategic vision that they’re after,” concluded Peck.

If you are interested in learning more about how to make wire transfers relevant and profitable, please fill out the form below to access Fiserv complimentary whitepaper titled “Four Trends in Wire Payments.”