Since the first mobile devices were enabled with contactless capabilities nearly a decade ago, contactless payments have been gradually gaining acceptance in the U.S. While early adoption has been led by younger consumers, the global COVID-19 pandemic has caused consumers of all ages to rethink the ways in which they pay, fueling even more rapid growth in contactless payments. Consumers are engaging in social distancing and focusing on their safety; they are more comfortable if they don’t have to touch cash or even keypads, so it’s not surprising to see them embracing contactless payments now more than ever.

To discuss the growth in contactless payments and how credit unions can best position themselves in the market, PaymentsJournal sat down with Jeremiah Lotz, Managing Vice President, Digital Experience & Payments Products at PSCU and Sarah Grotta, Director, Debit and Alternative Products Advisory Service at Mercator Advisory Group.

Trends in Contactless Payments

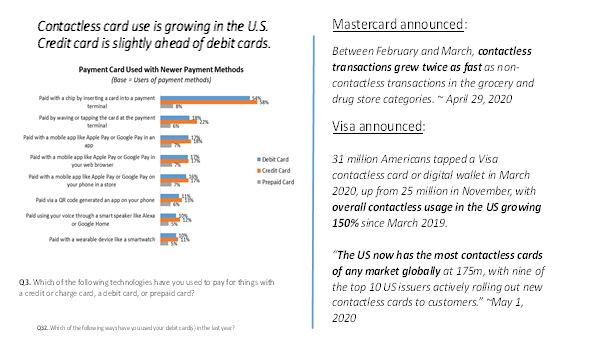

The chart below compares credit card and debit card payment options for contactless payments. The survey of over 3,000 consumers, conducted late last year, shows a slight preference for credit cards over debit cards in contactless transactions. “We find that wealthier individuals are more apt to use contactless and wealthier individuals are also more likely to use credit cards,” explained Grotta.

More recent statistics from Mastercard and Visa reflect the impact COVID-19 has had in the contactless arena. At the onset of the pandemic, Mastercard found that contactless transactions grew twice as fast as non-contactless transactions at grocery and drug stores, which were, of course, deemed essential and thus allowed to remain open throughout the nationwide shut downs.

Visa indicated that its contactless card and digital wallet usage was up 150% since March of 2019. It also noted that, “The U.S now has the most contactless cards of any market globally at over 175 million.”

With increasing consumer demand, there has been an increase in both the issuance rate and merchant acceptance rate of contactless products. Virtually all new POS systems are contactless enabled and businesses large and small are coming onboard. Digital transactions are not only being used in place of credit card transactions, but are starting to replace cash at the POS. Early adopters are getting into the habit of tapping and paying.

The digital shift encompasses more than just POS transactions. We are seeing an uptick in a range of financial activities including online bill pay, P2P transactions, and the use of digital devices to manage financial services.

Heightened health-related concerns stemming from the pandemic have accelerated a change in consumer behavior that was already well underway. “Obviously consumer preferences are shifting, and while I think it’s a result of what’s happening right now, I think it also will likely be a permanent shift,” noted Lotz. “I don’t believe that as we move more individuals to transacting contactless and using digital devices more, that we’ll step back.”

Contactless Payments Offer Security Benefits

Contactless payments are more secure than traditional magnetic stripe or chipped cards. For starters, there is no opportunity for skimming (swiping cards through a skimmer to capture and store account information) because there is nothing to swipe.

Account numbers are never stored on mobile devices. Instead, the account number is stored and transmitted in the form of a token, a string of undecipherable characters that is useless to anyone who might try to intercept it. Furthermore, tokens are linked to a specific device and cannot be used independent of the device.

How Credit Unions Can Meet the Accelerated Demand

Credit unions can take this opportunity to evaluate their strategies as a whole to determine how to provide the most benefit for their members and potential new members. “This is a great time to look at what your overall strategy is in regards to card issuance and reissuing contactless,” recommended Lotz.

Typically, new cards are issued over an extended period of time as old ones expire. While this is the easiest and least expensive process, expediting distribution to get new cards into consumers’ hands sooner might prove to be the better solution. Credit unions need to figure out the best strategy for their members based on their individual needs.

Top-of-Wallet Strategies

The key to maintaining top-of-wallet status is keeping up with consumer trends, figuring out what consumers most want and providing a solution that meets their needs and expectations. This is no easy feat.

- Tools

Credit unions need to provide a comprehensive package that offers more than just the speed and convenience of contactless cards and payments. Digital management of the account adds substantial value.

Enabling alerts allows transactions to be monitored in real time so that every transaction can be verified and any potential problems are caught immediately. Controls can be set to help manage spending by setting limits and prioritizing purchases.

- Communication and Education

Many potential users are reluctant to try contactless solutions because they don’t have enough information to make an informed decision. It is important to take the time to educate consumers, to make sure they understand what they’re looking for, and how the card works.

Well publicized security breaches that have exposed account information in the past have made many people more cautious in their financial dealings. Explaining the security features that make contactless transactions even more secure than traditional cards can alleviate customer concerns.

Finally, keeping in mind that individual needs and circumstances vary and one size doesn’t fit all, providing a review of all available options will lead to greater customer satisfaction and retention.

- Fraud Protection

Stopping fraud before it happens is the ultimate goal, but customers need to know that, in the unlikely event that fraudulent activity does occur, they will be protected. Putting procedures in place and clearly communicating those procedures to customers lets them know that they can trust their credit union to keep accounts safe and to quickly and efficiently rectify any problems that may occur.

- Rewards

Rewards and incentives are a key factor in deciding which card to use. Cards that offer rewards such as cash back, gift cards, and travel rewards are more often the go to card.

Conclusion

Credit unions are dedicated to serving their owner-members. They are known for their personalized response to member needs, high level of customer service, and community involvement. The contactless arena presents an opportunity for credit unions to shine.

According to Grotta, “this is starting to become a widely accepted, very available solution.”

The speed, convenience, and security of contactless transactions will help it maintain top of wallet status. Now is the time for credit unions to start to think about and plan for contactless solutions.

PSCU has enabled a number of credit unions already and has the knowledge and experience to provide strong leadership. “We’re in a position to make sure our credit unions clearly understand and have a strategy; we’re there to consult with them on which portfolio, and which method for each of those portfolios, makes the most sense. But now is the right time to have the conversation,” concluded Lotz.