Financial institutions have traditionally been risk-averse, relying on tried-and-tested products and services. However, transformative innovations—such as real-time payment rails, artificial intelligence (AI), ISO 20022 adoption, and increasing demands for cybersecurity and fraud management—along with a constantly shifting regulatory backdrop—are making it critical for organizations to adopt new technologies.

In a recent Payments Journal podcast, Radha Suvarna, Chief Product Officer for Payments at Finastra, and James Wester, Co-Head of Payments at Javelin Strategy & Research, discussed the trends shaping the financial services industry and how organizations can seek new opportunities while keeping security and compliance top of mind.

Resilience Amid an Unpredictable Future

One of the main trends impacting the financial industry is the growing expectation—among customers, partners, and regulators—of what a bank should be.

“Let me call it resilience,” Suvarna said. “Given the growth of real-time payments globally and the criticality of payment infrastructure to the local economies in many countries, we are seeing a lot of regulators who are starting to expect more from banks, both in terms of platform availability as well as disaster recovery requirements. In turn, expectations around 24/7 service and responsiveness have increased.”

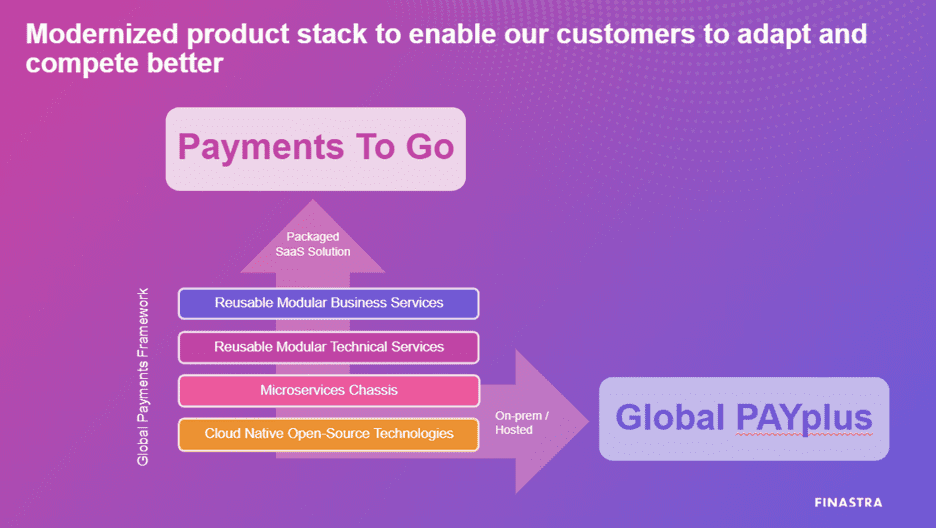

Finastra has developed our Global Payments Framework (GPF) to underpin the modernization approach for our suite of payments and financial messaging products (see below).

Many small to mid-tier banks are unprepared for new payment formats coming down the road, such as ISO 20022. This makes speed to market increasingly important, allowing these banks to comply with the new specifications before they become mandatory.

Another trend impacting the industry is the move to combine multiple rails into a single payment hub. This approach centralizes a financial institution’s payment processing, simplifying the technology stack, streamlining operational processes, and enabling innovative use cases.

At a broader level, organizations across industries are adopting cloud-based solutions. In the financial sector, banks and credit unions of all sizes are leveraging these platforms to move away from costly data centers. Instead, a technology vendor can manage the payments orchestration end to end.

Another overarching trend is the adoption of generative AI in various forms. For example, Agentic AI solutions are both enhancing the customer experience and improving operational efficiency.

Whilst the potential of these trends is clear, navigating the path to adoption can be extremely challenging.

“There’s so much complication on the business side, and now the technology departments are being told you need to be ready to do all of this. Also, can you anticipate everything that’s going to happen in the future?” Wester said. “With things like Gen AI, do we really know exactly what’s going to happen with that? No, we don’t. You now have to future proof against a future that used to be somewhat predictable, but now is completely unpredictable.”

Playing Offense with Payments Modernization

Though these emerging payments technologies may seem daunting, they are ultimately just tools that financial institutions can use to fulfill one of their most fundamental functions: moving money from one account to another.

With this mindset, organizations can begin to break down the elements of payments modernization that will have the greatest impact on them.

“In my mind, the business case and the business value around modernization should be seen in two lenses—I would call them offense and defense,” Suvarna said. “On the offense side, modernization should drive product innovation and enhance the customer experience, whether it’s faster and immediate funds availability for cross-border payments, greater transparency, or a reduction in cost.”

An example of playing offense would be embedding payment initiation within a customer’s ERP system. In the past, users may have had to upload files with batches of payments to the bank’s website. If customers were able to integrate payment initiation directly inside their ERP systems, it could be a game changer in many use cases. Also, a highly configurable solution means banks can avoid risky and expensive customizations, allowing them to introduce new rails, features, and process payments around the clock without upgrading the entire payments system.

Another way to play offense is by incorporating intelligent payments routing, or smart routing. When multiple payment mechanisms are available—such as a real-time payments or wire transfers—smart routing can help determine the best option based on a wide range of criteria such as speed and cost.

This same principle can be applied to cross-border transactions, which have traditionally been a pain point in payments. Smart routing technologies could evaluate options like Swift, Visa Direct or Mastercard Move to determine the best way to send the payment.

Another offensive maneuver could be streamlining the payment reconciliation process. For instance, ISO 20022 has a flexible and XML-based structure where the invoice amount, invoice number, and other data can form part of the transaction payload. This additional information can make it much more efficient to reconcile payments and invoices; or automate the process completely.

“The next stage is how do we leverage the specification to drive incremental value to the customers, and go after the customers that the banks don’t have today?” Suvarna said. “All of that is possible through modern technology and architecture. That’s all offense—to drive incremental market share and incremental customer and business value.”

Protecting Against the Downside

Though it is critical to be proactive to stay competitive, financial services organizations can’t forget their foundations.

“At the end of the day, financial institutions are about compliance,” Wester said. “They are about risk management, governance, security, and all those things have reasserted themselves. We want to bring in new clients and deliver them delightful products, but still—as a financial institution—you need to be paying attention to those things.”

Defending against the downside means that financial institutions must stay abreast of new regulations, which are constantly changing. For example, as real-time payments become more prevalent, they will likely be governed by a more stringent set of rules than those that apply to other payment types.

This is because when an instant payment is sent, it is irrevocable. In contrast, the delays inherent in ACH transactions allow for payment to be reversed in cases of error or fraud.

Fraud, scams, and the increasing sophistication of cybercrime are critical threats to all organizations, but especially to financial institutions. That’s why building and maintaining strong fraud prevention capabilities is an essential part of playing defense.

“That’s the number one topic that we hear from both financial institutions and vendors now is that discussion on risk, compliance, governance, security, and they’re all changing very quickly,” Wester said. “Those same macro trends and micro trends apply to what bad guys are doing and how they can do what they’re doing, and the risks that are in the market.”

A Maniacal Focus on Customer Value

These risks, coupled with an uncertain future, have kept many financial institutions on the sidelines, waiting for a moment when it might be more convenient or less expensive to modernize their payments stack. However, institutions that delay modernization now will be even less prepared for what comes next.

“It’s exciting times, but it means that this is one of those things where I like to say, ‘There is no destination, it’s all journey,’” Wester said. “You’re never going to get to the point where you can say, ‘OK, we’re modernized, we don’t have to deal with this anymore.’ Understand that everything is changing, is going to continue to change, and over the horizon there are going to be more changes.”

In this shifting landscape, the first step in the payments modernization process is to embrace the change, get comfortable with it, and adapt the mindset to deliver value around the unique business and customer needs that a modern, agile solution can address.

“There is no one-size-fits-all solution in my view, but customers want scalability that is hosted by the vendor,” Suvarna said. “It’s more modern, resilient, and multitenant, which makes it a bit more cost effective for them. We need to adapt the modernization agenda, an objective that is number one.”

Once these needs are clear, financial institutions should explore how they can leverage partnerships and third-party solutions. For example, a cloud-based platform like Finastra’s Payments To Go, hosted on Microsoft Azure and designed for mid-tier banks, can serve as a plug-and-play solution, offering institutions scalable, secure, and around-the-clock functionality.

Partnering with a robust payments modernization provider can take the heavy lifting off financial institutions, allowing them to refocus on what they do best.

“Above all, it is critical to maintain a maniacal focus on delivering customer and business value, whether it is internal stakeholders or external stakeholders, and avoid distractions from the next shiny object,” Suvarna said. “Having a deliberate strategy, sticking with it, and keeping the eye on the ball is going to be critical. That approach ensures the best modernization outcomes for the institution and the customers we serve.”