COVID-19 hit every corner of the world, and people around the globe had to alter their everyday behavior in some way. The most noticeable change was limited day-to-day in-person interactions. As a result, people turned to technology for things like grocery shopping, cinematic experiences, and even banking.

With this sudden surge in an already tech-saturated society, the on-demand mentality of everyday consumers grew stronger. This way of thinking reached the world of payments, with apps such as Venmo and PayPal leading the charge. People began to expect immediacy when sending and receiving money.

To further discuss payments technology modernization and the importance of implementing real-time payments for banks and credit unions, PaymentsJournal sat down with Mark Ranta, Payment Practice Leader at Alacriti, and Sarah Grotta, Director of Debit and Alternative Products Advisory Service at Mercator Advisory Group.

Payments technology modernization

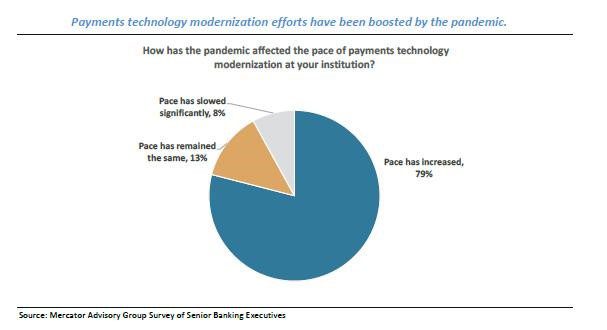

In late March 2021, Mercator Advisory Group worked with Alacriti on a survey of about 100 senior level bankers—19% of whom were from community banks and credit unions— focusing on their latest approach to payments technology, including real-time payments. One of the first questions asked is shown in the graph below.

The results of the survey show that nearly 80% of bank and credit union executives found that the pace of payments technology modernization picked up significantly as a direct response to the pandemic, while only 8% believe the pace has slowed down. This could be due to a number of factors, including the necessity to serve customers when branches were closed and a need for more automation in the back office to compensate for absent workers.

“For some financial institutions, this meant that they really focused their resources on modernization plans that they had already had in place, but were speeding up their efforts,” said Grotta. “And some took the opportunity to reprioritize payments modernization, maybe over some of the other activities they thought they were going to accomplish.”

With COVID-19 pushing payments technology years into the future, banks are seeing the importance of faster and real-time payments. To avoid being left behind, the majority of them are looking to accelerate their initial plans.

A market leader for real-time payments

There are over fifty real-time payments systems live globally, including those in the APAC, European, and Latin markets. Many of these systems have been around for over ten years, but the U.S. system is lagging behind. So, where are we in the market, and who can we look to for guidance?

“I would [suggest] all the financial institutions in the U.S. to look abroad, looking into the APAC region, and looking at what use cases their ecosystems are using is a good place to start,” recommended Ranta. “I mean, from where we sit, we know that the U.S. market is more complex and [has] significantly more financial institutions and more pieces to the puzzle than anyone else.”

The Asian market has a lot of experience and best practices to draw from, and understanding how they have transformed their business—not just technologically, but internally—into a digital-first experience will help underdeveloped markets catch up to speed.

The U.S. is only four years into its real-time payments journey, but the infrastructure being used within the industry is nearly forty years old, with the ACH Network and Fedwire systems having been introduced in the 1970s. It’s no surprise then that many financial institutions feel discouraged by new technologies when their back-office systems are still running on COBOL.

“These digital experiences are demanding and we’re seeing more and more fintechs, and more and more technology vendors, really come in and start to enter into the space that was once peripheral to the bank, and [are] now directly targeting bank-like products,” added Ranta.

Banks must take caution and consider the consequences of failing to act now, and move forward with an eye toward innovation.

Legacy systems vs. a cloud-based approach

Not too long ago, many financial institutions believed they would never put their infrastructure on the cloud. But as technology evolved, the stigma around public and private clouds has dissipated. Now, even the largest financial institutions around the globe are running applications on the cloud.

“Now, not to say they’re going to move their core to the cloud right away,” explained Ranta, “but realistically, I think that argument of on-premises built/deployed versus cloud really is kind of in the rearview. I think even up to the largest institutions, they’ve realized the value that the cloud brings, and the idea of not having to think about these large investments that have to be made.”

When considering infrastructure, one must consider technical debt that comes along with legacy systems. Tech debt is an inhibitor of advancement and innovation because the cost of an on-premises deployment system is significantly higher than one that is cloud-based.

Ranta believes that cloud offerings are the way to go because the cloud can scale as demand on the infrastructure begins to grow. With the cloud, financial institutions can pinpoint specific customer segments that they want to target and execute the deployment of the software for a low-level investment.

“When you don’t have to go through these massive business cases and all the things that we as bankers look at in the industry…that old model of thinking about projects and thinking about how to do things [can be] put into a box and moved to the side [so that banks can] move forward to innovate,” concluded Ranta.

A real-time payments road map

A major hesitance of real-time implementation for financial institutions is the idea that their infrastructure has to be ripped out and replaced, but the ‘digital bank within a bank’ isn’t an uncommon trend. Ranta advised bankers to innovate first, then adapt their processors, and lastly, migrate their systems.

The process of migration is not a single project, and financial institutions can expect to be on a real-time payments journey for the next five to ten years. More importantly, however, banks should not hesitate to begin to incorporate these new technologies. “Most banks have sped up their transformation plans, and that’s a good thing,” assured Ranta.

Mass adoption is expected to occur at a rapid pace, with all of these services and real-time payments starting to hit their stride. Anyone looking to educate themselves on the services offered can go online, download an app, and begin to interact with it.

“There’s plenty of closed loop systems and applications that sit on top of our banks today that you can play with to understand these [services] better,” insisted Ranta. “Roll up your sleeves and try them out internally. Think about these as being able to look at individual use cases you could innovate in and around and then expand within the FI.”