Payment facilitation, or PayFac, is quickly becoming table stakes for many merchants. With new technology diversifying payment methods across all industries, merchants are clamoring for streamlined payment acceptance functionality. Businesses are increasingly looking toward independent software vendors (ISVs) to provide those services, and those ISVs want to deliver fast and easy payment acceptance activation to their merchant partners through Software-as-a-Service (SaaS) offerings.

To learn more about the growing trend of ISVs implementing PayFac platforms to bundle payment acceptance into their software, PaymentsJournal sat down with Jareau Wadé, Chief Growth Officer at Finix; David Dew, Senior Manager of Digital Acceptance at Discover Global Network; and Don Apgar, Director of Merchant Advisory Services at Mercator Advisory Group.

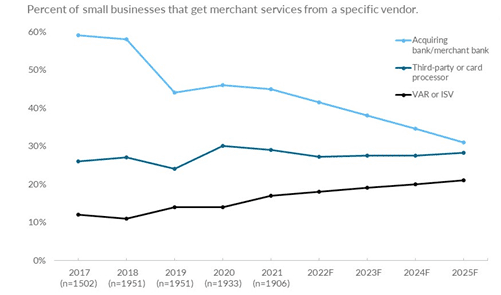

The Shifting Provision of Merchant Services

Over the past several years, there has been a steady decline in the number of businesses obtaining merchant services from their local bank or acquirer and a commensurate rise in businesses getting solutions from software providers. “This is part of a bigger trend that we’re tracking,” explained Apgar. “What we used to call a ‘merchant account’ is now less of an account, per se, and more of a software feature.”

This trend makes perfect sense when one considers the concurrent growth of SaaS as a business model over the past decade or two. “Combine that with the ease of accepting payments that has happened both on the consumer side and the infrastructure side, specifically when it comes to payment facilitators,” said Wadé. The result is small and midsize businesses (SMBs) primarily obtaining financial services through software providers.

Vertical Software-as-a-Service

The concept of vertical SaaS—providing software for all elements of one industry—is becoming more popular as a business model. “The average number of SaaS providers that a small business uses to run their company is seven, and some obviously use more,” noted Wadé. “What that means to me is that the vertical software companies like the ones that Finix supports have an opportunity to simplify business for their SMBs.”

Wadé continued: “If you can become the system of record—starting with payments, and then layer on things like tip management, payroll, etc.—that is going to allow you to be the bedrock of how these SMBs run their company…. I wouldn’t be surprised if the majority of consumers and merchants get their financial services in the future through SaaS companies.”

SaaS represents a true democratization of technology; even very small businesses can access solutions on a pay-as-you-go basis. “The influx of software companies has really transformed the payments industry,” Dew emphasized. “More and more of these vertical SaaS companies are embedding payments into their offering, and by working closely with partners like Finix, [Discover] is getting a much better understanding into the growth of payment facilitation within this segment and beyond.”

PayFacs: If You Can’t Partner With ’Em, Become ’Em

There are a variety of ways for SMBs to take advantage of payment facilitation. Legacy models such as referrals from independent sales organizations (ISOs) are still options, though those who use that method may find themselves at a disadvantage from parties who have done PayFac integration themselves, either by outsourcing to a dedicated PayFac or converting the business into a PayFac.

“There has been a renaissance with mobile technology and SaaS in general,” Wadé pointed out. “At Finix, what we are seeing is companies coming to us to become PayFacs, but also folks who have that aspiration someday and want to get started with something that might be a lighter lift, that still provides the path towards greater economic benefits and more control of the user experience.” Many SaaS users are pushing companies in that direction simply because it is so much easier to bundle everything in one place with an ISV.

“Pizza-as-a-Service”

Finix has developed a metaphor to describe different payment integration models, intriguingly referred to as “Pizza-as-a-Service.” Wadé broke down the options:

- Dining Out: ISO model. Less effort but with a recurring cost and less control over the final product.

- Delivery: Outsourcing to a PayFac. Delegating the work but bringing the service home.

- Take & Bake: Akin to DiGiorno®. Higher initial investment in pre-made parts but with in-house assembly.

- Made at Home: Developing and building payments facilitation entirely in-house, soup to nuts.

The idea of tackling payment facilitation entirely in-house may seem appealing at first—until companies learn that between PCI and OFAC compliance and software development for screening, dispute management, settlements, reconciliation, onboarding, etc., the time to market would be about 18 months (eons in the SaaS world) at a cost of $2–$3 million, plus several hundred thousand dollars on a regular basis for maintenance.

“[SaaS companies] really don’t want to be in the payments business, but they want to offer payments,” Apgar stated. “Outsourcing some of that would be a tremendous advantage for some of these SaaS companies.” Using a company like Finix to develop a payment stack means ISVs, SaaS providers, and value-added resellers (VARs) can outsource much of the cost, increase speed to market, and retain more control over the services they provide to SMBs.

Boosting Business with a PayFac Model

Both Finix and Discover work closely with Passport Parking, a notable use case for payment facilitation. Passport, which offers ticketing solutions for different cities and municipalities, was managing 22 different payment gateway integrations once upon a time. PayFac integration with Finix allowed Passport to get a distribution deal with Google Maps.

“That is the benefit of owning your own payments,” clarified Wadé. “You bring it in-house, even if you are outsourcing parts of the infrastructure to a partner, and you still have much more control of your destiny.” Moreover, such a model lowers the opportunity cost and frees up internal resources for core projects and expansion.

“Emerging technologies have really layered payment processing when you compare it to the traditional acquiring model,” Dew concluded. Integrated payments have become a necessity for SMBs, and a streamlined payment stack provided by a trusted partner makes business operations that much easier.

To learn more about including payment facilitator capabilities, read Discover’s whitepaper here.