Disbursing funds in an efficient and accessible way is critical to a good customer experience. But new economic realities and mobile adoption have challenged organizations to evolve how they pay to meet consumer demands.

In a recent PaymentsJournal podcast, two experts from Blackhawk Network, Sarah Kositzke, Director of Research, and Scott Lapp, Director of Product Marketing and Incentives, along with Jordan Hirschfield, Director of Prepaid at Javelin Strategy & Research, discussed the latest research on consumer payments preferences. The conversation focused on Blackhawk’s research into business-to-consumer disbursements.

Defining the Terms

Disbursements are typically issued when a customer is owed a credit or refund. Examples include a property management company returning a security deposit, or an airline handing out compensation because a flight was canceled. Blackhawk wanted to better understand customers’ payment preferences, specifically in terms of their banking classification —whether unbanked, underbanked, or fully banked.

According to the FDIC1, the fully banked—representing 80% of U.S. households—have established relationships with banks and use them for all types of services. About 5% of U.S. households are unbanked, meaning they do not have any established relationship with a bank. The remaining households are underbanked: They have a checking and/or savings account with a bank but also leverage other nonbank transactions, like those through rent-to-own services, payday loans, pawn shop loans, and tax refund anticipation loans. They are likely to be 34 and under, Black or Hispanic, have a high school education or less, and have a household income of $50,000 or less.

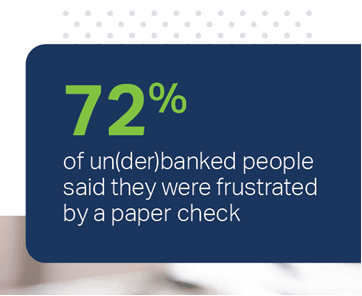

Strong Feelings About Printed Checks

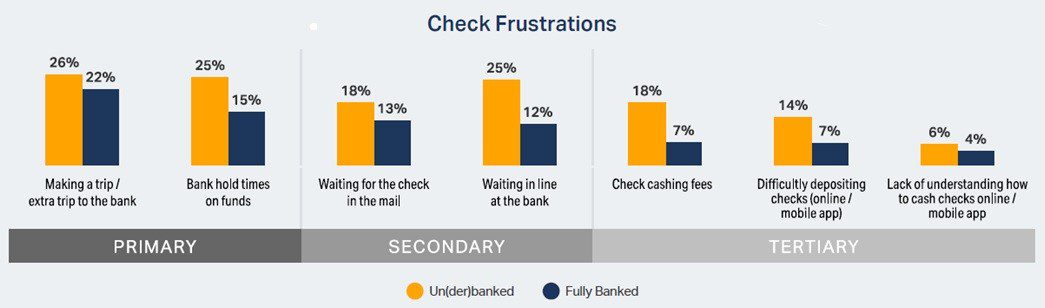

One of the strongest results from Blackhawk’s research was consumers’ antipathy toward physical checks. Nearly three-quarters of those in unbanked and underbanked households said they were frustrated by receiving a paper check. But nearly half (48%) of the fully banked households are also frustrated by receiving a paper check.

Much of the frustration around checks is that they are a small but real burden.. “Even to deposit a check via mobile phone, you have to set aside time to do that,” Lapp said. “If you’re not using mobile banking, then you have to find a bank or an ATM. Sometimes the person needs to go to the issuing bank, and if there is no local branch, they may have to go to a check-cashing place, which means paying check-cashing fees. And depending on the size of the disbursement, there can be a hold time on those funds.”

According to Hirschfield, Javelin’s research shows that 92% of adults have a checking account. “But even with those checking accounts, most of the money is moved in a card-based or digital format,” Hirschfield said. “Even as they’re making payments, not just receiving payments, they want to use a non-paper-based method.”

Payments You Can Feel Good About

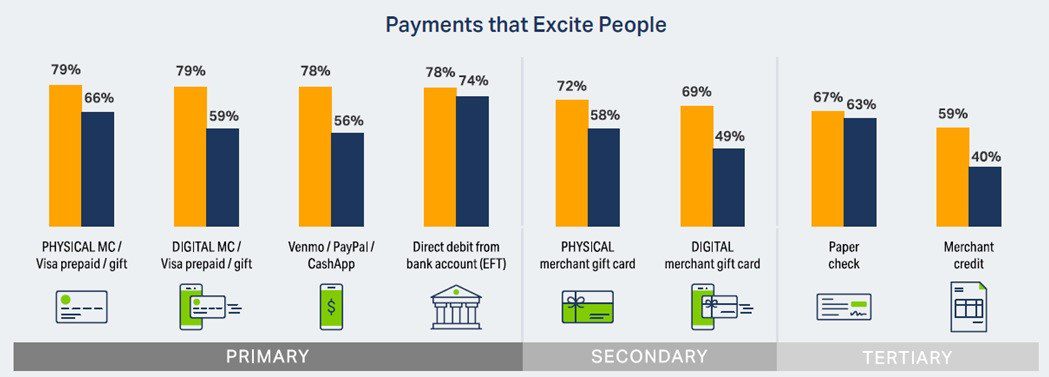

People are most excited about disbursement payments that are flexible and convenient—and that encourage them to splurge. The most popular methods include physical and digital gift cards; payments through vehicles like Venmo, PayPal, and Cash App; or directly deposited funds.

“We asked people about their ‘emotional payment connections,’ which is not something usually under consideration when sending a payment,” Kositzke said. “When selecting a physical or digital prepaid card from Visa or Mastercard, or a merchant gift card, these are viewed as treats that allow people to splurge on things they want. It’s splurging for the new dress, shoes, books, a night out. Other payment types, like a paper check, direct deposit, Venmo or Cash App were seen as a way to pay for things they need, like rent.”

Blackhawk found that gift card recipients often plan to spend more than the value of the gift card. If they receive a card valued at $50, on average they will spend nearly $60 beyond the value. If they receive a card valued at $500, they will spend slightly more than $100 beyond the value on the card.

“We agree from our own research that gift cards prompt additional spending,” Hirschfield said. “About 40% of consumers will generally spend more than they typically would when using a gift card, and 25% will generally purchase a more expensive item than they normally purchase.”

Physical or Digital

Blackhawk also asked customers whether they preferred a physical or digital disbursement. Fully banked customers split 50-50 on whether they would prefer a physical payment, but two-thirds of the unbanked and underbanked respondents preferred digital delivery. If the value of the payment is close to or more than $200, most people prefer digital delivery. Javelin’s research shows that although volumes are significantly lower on digital cards, which make up 28% of all cards, the average load values are significantly higher, at $115 versus $95 for physical cards.

The least desired form of disbursement, according to Blackhawk’s research, is a bill credit. Bill credits are often viewed as simply a way to pay for things. If the person is not paying close attention to the monthly statement or credit card bill, the credit may not even be noticed.

People were also surprisingly open to sacrificing some of the funds to receive their payment faster, especially among the underbanked population. Nearly a third of underbanked people were willing to give up between 1% and 3% of that payment to receive it faster. The fully banked were less enthusiastic, but 13% were willing to sacrifice at least 1% of those funds to get it faster.

Key Takeaways

Behavioral factors should never be dismissed by those working with disbursements. It’s critical to understand whether your payment is likely to be considered a reward or a treat, and those notions can be reinforced by issuing something like a prepaid gift card. People will likely splurge with that payment type, spending up to twice the card’s value.

It’s also important to consider the friction that printed checks cause, even for the fully banked. And keep in mind that bill credits are the least desired form of payment. “Emotional payment connections” may be largely overlooked factors in disbursements, but they can have a huge effect on how those payments are used once they are received.

1Source: Federal Deposit Insurance Corporation (FDIC), 2021 FDIC National Survey of Unbanked and Under-banked Households (October 2022)

To learn more, download the eBook: B2C Payment Preferences: How people want to receive payments

Let’s Start a Conversation!

Fill out this form to talk to BHN:

|

Your form has been submitted! A BHN team member will be in contact with you to learn more about your audience, objectives and needs. |

|