There is a common misconception that today’s bank and credit union customers want to do everything in a digital channel. The fact is that when it comes to financial services, consumers often have high expectations: in-person assistance when help is needed, plus the convenience of on-demand, self-service digital and mobile channels. How can retail banks and ATMs help meet these expectations?

ATMs play a key role in delivering this experience. Specifically, interactive ATMs that can handle most of the basic transactional work typically done in branches by tellers, such as check cashing, withdrawals with multiple denominations, account transfers, loan payments, and more.

To find out more about how ATMs play a role in a financial institution’s overall channel strategy, PaymentsJournal sat with Brendan Watkins, VP of Product Management at Fiserv, and Sarah Grotta, Director of Mercator Advisory Group’s Debit and Alternative Products Advisory Service.

Faciliating Consumer Choice

ATMs can play a key role in facilitating and offering choice to consumers, especially Millennials. Watkins noted that ATMs are a key touchpoint for Millennial consumers, and that, contrary to the popular belief that this cohort does everything digitally, physical cash still plays an important role in their lives.

“More than anything, Millennials really want choice,” he said.

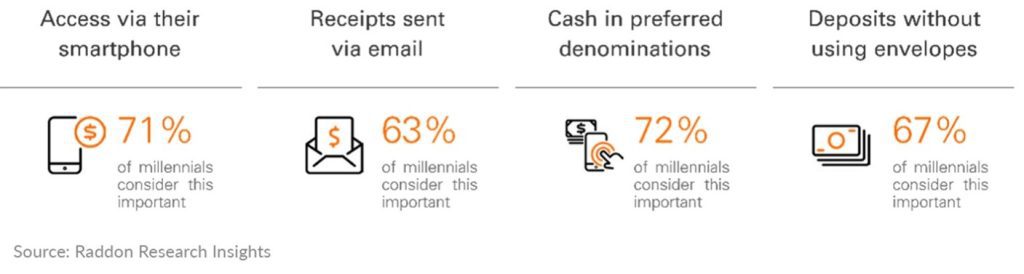

Grotta agreed, noting that Mercator research shows that Millennials do use cash and go to the ATM frequently. Research also shows that they are less concerned with paying surcharges, and more interested in choice. For example, Mercator research found that 72% of Millennials say that receiving cash from an ATM in their preferred denomination is important.

“Offering that choice is a big winner,” said Watkins. “Letting them get fives instead of tens or twenties is a great pleaser and incentivizes them to go back to that ATM.

Other ATM features Millennials deem important include the ability to receive an emailed e-receipt and accessing ATMs via a smartphone, according to Mercator research.

Specifically, consumers are drawn to cash for low-value transactions. Mercator research reveals that cash is used 49% of the time for payments valued at less than $10, and for 35% of transactions of any value conducted in person.

Creating More-Efficient Branches

Interactive or “smart” ATMs also enable branches to operate more efficiently. Watkins observed that some banks and credit unions are using interactive ATMs and other advanced technology to create a sort of hub-and-spoke model of branch distribution. In this mode, there is a “hub” full-service location providing the single best opportunity to display your brand and deliver a premium consumer experience. Here, all your technology and servicing should be on full display, addressing the needs of consumers who want and need the human touch, as well as those who want significant self-serving options. Supporting the hub are the spoke locations, acting more like a café in a given area, where customers can come in and have a cup of coffee and talk about financial planning with a representative. In these smaller locations, consumers can conduct basic tasks, almost entirely manned by video ATMs and other smart technology. They don’t even require employees to handle cash; that can be done by vendors coming in to service the ATM.

Grotta added that this model can help banks and credit unions fill gaps in staffing; with interactive teller machines replacing much of the function of human tellers, financial institutions can then redeploy budget to hire in other areas.

“This is especially important because staffing and hiring is so competitive these days,” she said.

This also enables banks and credit unions to free up their staff to do more exciting and valuable work than just processing transactions, Watkins said.

“It offers a different type of employment opportunity for associates because they are less transaction-focused and more focused on building relationships with customers,” he added. “You also are able to attract a higher-quality associate. Associates are excited to do less rudimentary tasks.”

This ultimately allows banks and credit unions to operate more efficiently and effectively without drastically increasing budget. Where ATMs are connected to core account processing systems, Watkins noted some institutions are seeing a reduction in branch wait times Another example Watkins cited is creating longer hours for some branch locations. For locations that are transaction-based and mostly staffed by video tellers, banks and credit unions can deploy workers from different time zones or locations to work at different times to ensure the location is open longer than the typical nine-to-five hours.

“It gives you flexibility and the ability to create a remote workforce,” said Watkins.

Deepening Customer Relationships

Modern, interactive ATMs can also be connected with a financial institution’s core systems in order to deepen customer relationships. Watkins noted that Fiserv is uniquely positioned to do this, as it is also a core provider and has a robust card services program as well. He said interactive ATMs can be connected to core systems via APIs, which “lays the groundwork for future possibilities as well.”

This turns ATMs into more than just mere cash dispensers, but full-fledged customer touchpoints no different than the mobile or online channels.

For example, the ATM can be connected with CRM systems so that consumers’ full financial picture with the institution is known at the time when they interact with the ATM.

“So, you can deliver a targeted offer right there, similar to what we might do in online banking,” Watkins said.

Grotta compared this ability akin to what is happening in the realm of super apps, where a multitude of features are offered through a single app.

“You pool together more functionality and more of a consumer’s financial history and background into one single place,” Grotta said.

Another key advantage of modern, smart ATMs is that they can be serviced remotely, Watkins said, which means they can be repaired quicker as opposed to having to wait for someone to come in and physically fix the machine.

“It really helps with your ATM fleet uptime,” he added. “It greatly increases ATM availability.”