Payment choice is increasingly driven by two critical factors: security and convenience. As consumers adopt new payment technologies and digital channels, financial institutions must balance seamless user experiences with robust fraud protection. Research from PSCU’s Eye on Payments study highlights how concerns about card fraud, identity theft, digital payment security, rewards, and ease of use continue to shape consumer behavior. Understanding these preferences can help credit unions and financial institutions strengthen member engagement, improve payment experiences, and adapt to evolving payment trends.

Subscribe to our podcast via:

The following is a transcript of the podcast episode:

Brian Riley, Director, Credit Advisory Service at Mercator Advisory Group

Welcome. Today we’re going to be talking with PSCU. One focus is a recent report from PSCU’s Eye on Payments study. I’d like to kick off our discussion by asking Tom a question. What’s interesting about the report is it centers on two factors that drive consumer choice, which are safety and convenience. Let’s focus on safety for a moment because with all the data breaches we see in today’s world, that’s something that’s on just about everybody’s mind.

So Tom, what do you think are the top findings from the report?

Tom Pierce, Chief Marketing Officer at PSCU

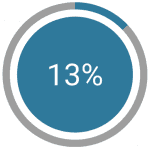

Thank you, Brian. We did find that security, safety, and the convenience factors were the top drivers of payment choice for both credit union members and nonmembers in terms of what type of payment – debit, credit, digital, cash – they used in different formats. This was severely impacted by what we saw in terms of the number of folks that had been impacted in some way [by a data breach] in the survey period. We found 13 percent of credit union members had experienced some type of card fraud and we found that 4 percent had had their ID stolen. This was really apparent across the different generations, particularly as we looked at the Boomers, the Gen Xers, and the older Millennials. All of them had reported some sort of card fraud as the leading incident for them in the past six months to a year. So it really has impacted their decision-making process for payments.

Brian Riley, Director, Credit Advisory Service at Mercator Advisory Group

Sure, and when you think of the number of even disputes that come in. We did a recent study on disputes and found about 25 million disputes coming through transactions. And we also find that one of the big saving factors is when customers are alerted through a regular online feed. If you just made a transaction, you get an alert “Was that you?” But it’s amazing how it really impacts so many different customers.

Sarah Grotta, Director, Debit and Alternative Products Advisory Service at Mercator Advisory Group

And certainly I think on the debit front we’re seeing more fraud in debit card on the card-not-present front and that is interesting. It’s obviously a bad sign, but it’s a result of debit card consumers getting a little more comfortable utilizing their debit card in card-not-present environments. But it also represents an opportunity too for credit unions, and for any issuer quite frankly. Brian, you were talking about getting alerts and most institutions have alerts and some have controls, but we find that the utilization or the engagement around those solutions is a little low. So it’s an opportunity to market them and to get that engagement going to really make them effective.

Ivana Spadijer, Manager, Fraud Product Strategy at PSCU

I would agree. I would like to also add to that is that I think that we as an industry have done a fabulous job giving that peace of mind to our cardholders of that zero liability. For ages, we have always told them, “Don’t worry about your account. We have your back with zero liability.” To your point, Sarah, the industry has changed quite a bit and then with the newer technology like alerts and controls, it is definitely a great opportunity to go back to the front line and reeducate those cardholders to be more engaged with their account. That is one of our principles when it comes to fraud prevention here at PSCU as well. That is, the more that your member is engaged with their account, it’s another set of eyes that is protecting that account.

Brian Riley, Director, Credit Advisory Service at Mercator Advisory Group

One of the mantras of fraud too is that it always goes to the weakest channel. So when you think about what EMV has done, it’s done some really significant things as far as controlling counterfeit card fraud. And with that, crooks aren’t retiring. They’re just finding new holes. And that’s really one of the contributors of card-not-present fraud count.

Ivana Spadijer, Manager, Fraud Product Strategy at PSCU

Absolutely. You mentioned finding the weakest link. I’ll tell you just some of the things that are happening in the industry. You mentioned that EMV. EMV has done a tremendous job, and it certainly worked to reduce the amount of card-present fraud. But now fraud has moved to the card-not-present channel as well as other channels. I can tell you that some of the trends that we’ve seen over the past few years is fraud moving down the phone channel. Phone channel is very vulnerable. With all of the breaches we’ve had over the past years, whether it’s the Equifax breach or some of the government breaches and even five years ago the Experian breach, these fraudsters have enough information to authenticate. Therefore, they know that the phone channel has become the weakest link. They have ways to encourage that customer service agent who is trained and conditioned to provide the best customer service and not necessarily interrogate the caller. As a result, the phone channel has been one of those areas of vulnerability. This is why PSCU has been the first credit union service organization in the industry to deploy fraud detection on our phone channels, which we did by partnering with Pindrop. I will tell you that another channel where we have also seen a lot of fraud come through, apart from the phone channel and card-not-present channel, is on the digital side, getting access to the online banking accounts. Once the fraudster has the ability to have that access, they can do things like balance consolidations, which are very, very lucrative for the fraudsters. So that is another area where we’ve seen fraud.

Rewards is another channel that as a result of EMV stopping the card-present channel, it has moved these fraudsters to essentially purchase credentials on the dark web and therefore able to cash out on those rewards. Rewards are already very costly for a credit union to offer to members in order to retain their loyalty. Most of us as consumers typically do not monitor our rewards unless it’s time to actually cash them out, and the fraudsters know that. So, that is another channel where we’ve seen quite a bit of fraud and therefore we have some fraud protection as well. As a result of all of these different channels that we’ve seen fraud now traverse as a result of EMV, PSCU has deployed our Linked Analysis platform, which allows us to truly provide a holistic omnichannel fraud protection to link all of these different channels together in order to prevent that fraudster’s [attack].

Tom Pierce, Chief Marketing Officer at PSCU

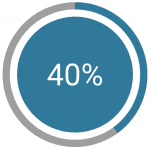

It’s interesting to tie back to the PSCU study, Ivana. She talked about the digital side. Our Eye on Payments study found that 40 percent of respondents to the survey said they really don’t want to use digital payment forms because they don’t trust them. So there’s an opportunity because they’re just as safe as the card but credit unions need to educate their members about the safety precautions to support them.

Brian Riley, Director, Credit Advisory Service at Mercator Advisory Group

There’s a lot of art and science that goes into fraud management. You could stop fraud if you shut down the authorization system. That’s a little severe for people who make money on payments. It’s a matter of how well you open those parameters up and manage things like false positives, and that’s really the shift between art and science in a fraud manager’s day.

Ivana Spadijer, Manager, Fraud Product Strategy at PSCU

Absolutely. It’s the constant balance of member experience and reducing that fraud.

Brian Riley, Director, Credit Advisory Service at Mercator Advisory Group

Well. Enough about gloom and doom and safety issues. Let’s talk about comfort and convenience. Tom, how did those factors fit into this whole play?

Tom Pierce, Chief Marketing Officer at PSCU

Clearly consumers want, what they told us through the study, both credit union members and non-members want choice. They want to use the most convenient payment form for them whether it’s in the grocery store or convenience store or even in paying a babysitter for that service. So they’re going to choose what’s most convenient. That factors in with security top choices. We also found that as you look at the credit card side – and credit card was the top payment form chosen for both convenience and safety and security across the board, across both audiences, both credit union members and nonmembers –on the credit card side, rewards played a factor as well. Ninety-three percent of credit union users said they receive some type of rewards or incentive for using that card when they’re paying. Six in 10 of those are getting some type of cash back. On part of the cards, 4 in 10 were having some sort of points opportunity. So clearly rewards are playing in as a factor. It probably falls into that convenience set as well though, Brian. It’s under that component, but rewards play a factor as well for the credit card user.

Brian Riley, Director, Credit Advisory Service at Mercator Advisory Group

One thing that always catches my mind with credit unions is the low rate of interest that is charged against the market. You know, typically it’s not unusual to see a range between 9 percent and 13 percent when the basic Chase Freedom Card is closer to 20 percent. So I think those factors play an important role and really the interest rates and the benefits of membership rather than being a customer that’s being profited by a major money center bank is a distinguishing characteristic.

Let’s give a few moments to debit. What surprising facts did you see out of the Eye on Payments debit study?

Tom Pierce, Chief Marketing Officer at PSCU

It was interesting there, Brian and Sarah, because this is one of the areas where there was a clear distinction between the credit union member and the non-credit union member, where debit is seen as a much better choice for making a payment, easier to use, something they’re comfortable using, convenient, fast transactions. The other factor that played in here that was distinct, particularly for the credit union members, is that debit cards allowed the credit union member to budget more easily. So if you think about the typical persona of a credit union member, they fit into that debit card persona probably a little stronger. And it’s reflected as PSCU serves our owner base, debit transactions are extremely strong still. That’s a big driving factor. So that’s really a distinction from the debit perspective.

Sarah Grotta, Director, Debit and Alternative Products Advisory Service at Mercator Advisory Group

We at Mercator Advisory Group are predicting continued strong growth in debit card transactions, which is interesting. But it does vary between some of the demographics and we do see that some of the older Millennials, where debit card is better received. Some of the information from your study can be helpful to some of your member credit unions to understand where to focus their marketing for debit card to achieve the greatest acquisition. To your earlier point, consumers really like choice. As the economy ebbs and flows, we do see that there’s this link between debit card use and credit card use and I think members who are really interested in being top of wallet with their customers regardless of what the payment choice might be for any given transaction, being able to offer all solutions – debit and credit as well some of the newer form factors – really helps to consolidate all payments with your member credit unions.

Tom Pierce, Chief Marketing Officer at PSCU

As mobile becomes more of a reality and more point-of-sale devices are able to accept that, there is going to be a need to push the credit unions to drive that security factor. It will be fascinating to watch in 2019 as contactless becomes more prevalent, especially on the credit side. I know that I heard you on your other presentation, Sarah, looking at contactless on the debit side probably is not going to happen in 2019 for most institutions because of the cost. But on the credit side, will the contactless be a catalyst to shift to the mobile device because of the ease of use, or will it be so simple to use, you just wave your card in front, that you don’t even shift to the mobile. It will be really interesting to watch the marketplace.

Brian Riley, Director, Credit Advisory Service at Mercator Advisory Group

And just when we retrained 400 million cardholders in the United States to dip their card, now it’s time to wave it.

Any other additions you’d like to mention while we’re all together?

Tom Pierce, Chief Marketing Officer at PSCU

I think overall PSCU is very excited to have a chance to do this deep dive in with consumers to learn what’s important for PSCU from an investment perspective to meet the needs of our credit unions and their credit unions and their members, and also for our credit unions to learn this information so they can decide which investments they should be making for the future to serve their changing member base.

We’re going to commit to do this study on an annual basis, and we’ll look forward to seeing how the trends evolve year to year.

Subscribe to our podcast via:

Conclusion

The study reinforces that consumers want payment options that are both secure and convenient. While fraud concerns remain a significant influence on payment decisions, consumers also expect flexibility, rewards, and frictionless experiences across credit, debit, digital, and emerging payment methods. For credit unions and financial institutions, success will depend on educating members about security features, investing in fraud prevention tools, and offering payment solutions that align with changing consumer preferences. As digital payments, mobile wallets, and contactless technologies continue to evolve, institutions that prioritize both trust and convenience will be best positioned to strengthen customer relationships and drive payment adoption.