The ways consumers purchase goods and services has been evolving in recent years, and COVID-19 has only accelerated the trend toward e-commerce with a number of innovations in tow such as Online Banking Payments, contactless payments, and buy now pay later options. For merchants, this evolution provides a great opportunity to offer payment methods that sit outside of traditional card networks.

To talk about consumer buying trends and why it’s time for merchants to think beyond card payments and its suboptimal 5-party model, PaymentsJournal sat down with Craig McDonald, Chief Business Officer at Trustly and Raymond Pucci, Director of Merchant Services at Mercator Advisory Group.

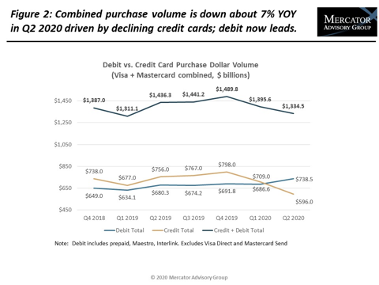

Debit has taken over top of wallet

In recent research, Mercator Advisory Group found that debit card use is increasing. Meanwhile, credit card use is declining. This has significant implications for merchants. “Consumers seem more comfortable now with making purchases that are charged right to their bank account, and a lot of that is driven by the pandemic,” explained Pucci. “Consumers do not want to have to make payments in the future.”

McDonald agreed, noting that Trustly has also found that consumers are utilizing debit as their top of wallet choice. The chart below, provided by Mercator Advisory Group, highlights the trend of debit becoming consumers’ preferred payment method:

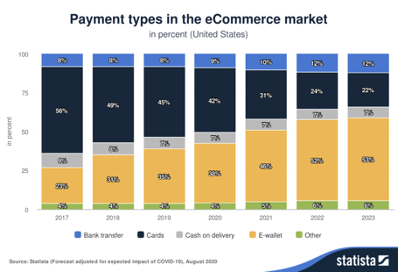

Other payment types are gaining traction too

First, e-wallet use has grown considerably in the last few years, and is anticipated to see more growth through 2023. Other payment methods, and in particular Online Banking Payments, are also gaining traction with North American and European merchants and consumers. The following Statista chart reveals what this growth could look like:

E-wallets aren’t completely separated from cards, as they still rely on consumers linking their credit or debit card to the account. “It’s really, from our perspective, a shift from cards to another form of card utilization via Apple Pay, Google Pay, Samsung Pay, or Amazon Pay,” said McDonald. The chart shows that card and e-wallet use is basically “flip flopping from 2017 to 2023,” he added.

Buy now pay later (BNPL) is also on the rise, as are Online Banking Payments or bank transfers through P2P apps like Venmo and Zelle.

While merchants have historically had limited options in terms of payment acceptance, 2020 has brought the necessity to evolve and optimize digital payment strategies in order to cater to the overwhelming shift to e-commerce. This opens the door for new innovations and payment alternatives from companies like Trustly.

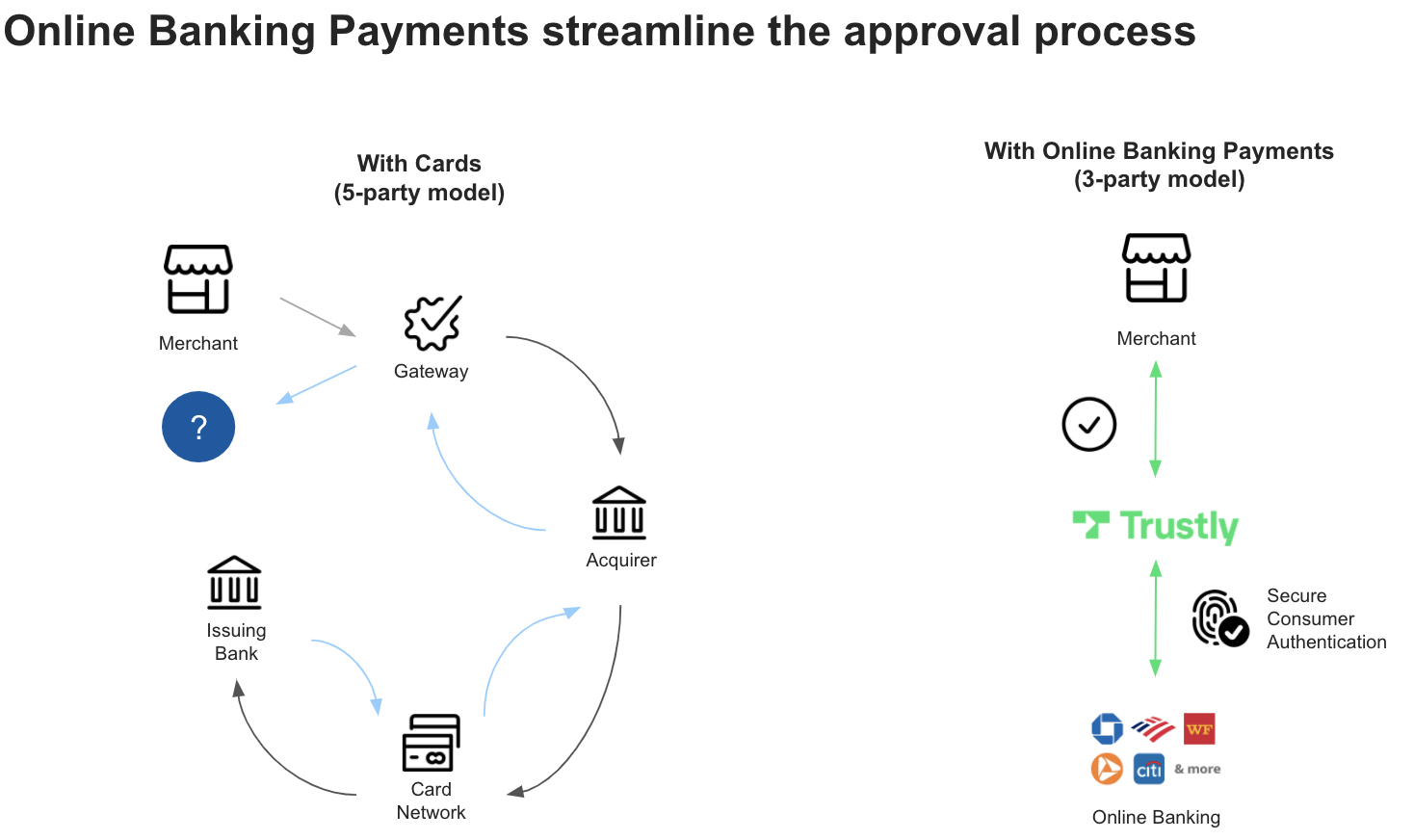

The legacy 5-party payment model is prone to operational error

The card model was built for card present transactions, but has challenges as an authorization method in an increasingly digitized environment with growing Card-Not-Present (CNP) transactions. The image below, provided by Trustly, depicts the traditional 5-party model for card transactions:

McDonald explained that, in a 5-party model, “the merchant, the acquirer, the network, and the issuing bank, in some way, shape, or form, are all looking and applying some risk rules and algorithms to determine whether this transaction and card being offered for utilization is coming from the consumer rather than a fraudster.”

This disjointed process results in weak customer authentication, which can lead to false declines and fraudulent transactions which result in chargebacks. This can mean a loss of revenue for merchants and a poor customer experience for consumers shopping online.

But this doesn’t have to be the case. “A streamlined authorization process will go a long way for merchants to retain most of the purchases that come through their online channels,” said Pucci.

Introducing Trustly’s 3-party model of Online Banking Payments

Knowing the shortcomings of the 5-party authorization process, Trustly created a way to authorize payments with just three parties: the consumer, the merchant, and Trustly. This model is also depicted in the above image.

Embedded within the 3-party flow is systematic and secure consumer authentication for each transaction. Consumers initiating payments simply login to their bank with the credentials they already know by heart and potentially enter a code for two-factor authentication.

“What we’ve done, and what is fundamentally different from the card networks, is that at that point in time we have verified with virtually 100% degree of certainty that this consumer is who they claim they are,” noted McDonald. “By the virtue of successfully logging into their online banking, we know again with virtual certainty that they are the owner of that underlying account with which they intend to pay,” he added.

Trustly has the same level of visibility as issuing banks and is able to use its streamlined process to receive an authorization request, enforce secure consumer authentication, and send an approval to a merchant in real time. A higher approval rating for merchants means more sales, fewer chargebacks, and less friction in the customer experience.

The takeaway

While the inefficiencies of the 5-party model are not new, they are even more important to address amid COVID-19 as merchants shift online to accommodate the surging demand of digital commerce.

With cash flow more important than ever, merchants can utilize Trustly’s Online Banking Payments solution to see cost savings of up to 50%. With a typical implementation pace of four to six weeks, merchants can get up and running with more cost effective payment processing in little time.